Author: David I. Templeton, CFA, Principal and Portfolio Manager

A confluence of factors came together a week and a half ago precipitating a crisis in the banking system, not only in the U.S. but globally. Three banks have failed in the U.S. in the span of about two weeks and, at the time of this writing, Credit Sussie in Switzerland is on the verge of being acquired by UBS due to operating issues. The three U.S. banks that failed were not involved in what most would consider typical lending activities. Both Signature Bank and Silvergate Capital were involved with companies in the crypto currency industry. SVB Financial Group (SIVB) and its Silicon Valley Bank dedicated a large percentage of its commercial loan activity lending to startup companies. A recent Wall Street Journal editorial ($$$) describes SIVB's lending activities,

"SVB was beloved for its willingness to offer 'banking services to startups that often weren’t profitable, in some cases didn’t have a product, and would otherwise have a hard time getting a line of credit or a loan from a larger bank.' One tech entrepreneur provided law.com a more scathing description of SVB’s products: 'They’re basically subprime business loans. You’re talking about companies that have no credit profile, they’re burning cash and are unlikely to raise the same type of capital because of interest rates.... It was basically social credit.'"

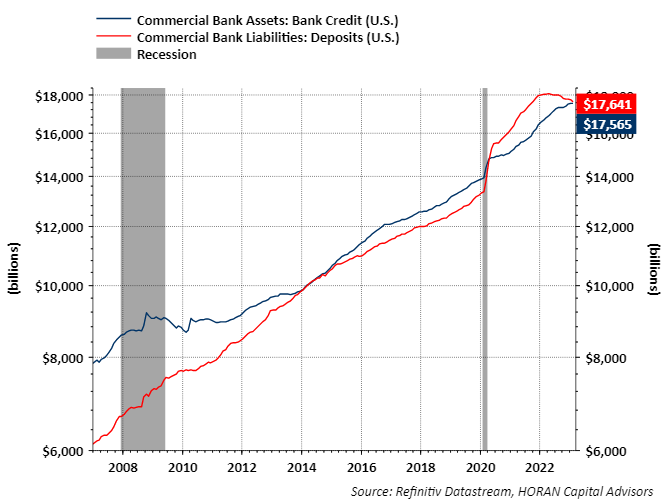

At the end of the day the pandemic that began in 2020 and the monetary and fiscal response by the U.S. government far exceeded what the economy needed. Too much cash in the economy not only led to higher inflation, but to balance sheet issues for banks. Specific to the banks was the fact they ended up holding too much customer cash and what was not lent to borrowers was invested in longer maturity U.S. government securities. Therein was the trap, customer bank deposits were short term instruments and the bonds were long term in comparison. As the Fed aggressively raised interest rates, the value of the longer-term bond investments declined. As short-term interest rates rose, the rate banks paid on bank money market accounts was substantially below what one could earn on a U.S. Treasury. Bank depositors took note and began to move money out of the banks in search of the higher yields as can be seen with the red line in the below chart. In order for banks to pay the depositors' funds, the government bond portfolios were sold at a loss.

Up to this point, the issues facing financial firms has mostly been a liquidity issue and not a credit one due to the mismatch of the bank's assets and liabilities. T. Rowe Price (TROW) published recent reports on these financial issues, U.S. Bank Failures: What Happened and What We’re Watching (PDF), that is written in a Q&A format and Bank Contagion Appears Limited, but Failures Create Key Risks, both reports are worthwhile reads for those interested.

Banks are much better capitalized today versus in the lead up to the 2008/2009 financial crisis. It would be surprising to see today's banking issues lead to a scenario similar to the 2008/2009 financial crisis period. The banks having issues now are those that surprisingly do not or did not have a handle on acceptable asset and liability management of the balance sheet. This is basic balance sheet management that banks should not struggle with implementing today. Also, as noted in the T. Rowe Price reports, startup firms and venture sponsored startups will likely have a harder time obtaining financing. This is not necessarily bad either. Maybe better discipline is followed in determining what an attractive start up is or isn't. Finally, other credit issues can develop in a slowing or recessionary economy. One to keep an eye on is downtown commercial real estate due to the continuing size of the work from home workforce. The real issue at the moment for banks seems to be one of confidence.

Disclosure: Firm/Family long TROW

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.