Author: David I. Templeton, CFA, Principal and Portfolio Manager

Recently, a number of mutual fund firms, Vanguard and Charles Schwab, to name a couple, are being forced to amend their prospectus around SEC diversification requirements for some investment strategies. In short, for a fund to be classified as diversified, the fund must invest no more than 5% of its assets in any single company and no more than 25% of the fund can be allocated to a large concentration across ten or fewer stocks. This is now an issue facing S&P 500 Index investment strategies.

With today's market index return concentrated in a small number of stocks like the Magnificent 7 (MAGS), this has led to fund companies managing capitalization weighted S&P 500 Index funds needing to inform investors the index fund is no longer diversified. With the fund not classified as diversified, the fund company is able to maintain investment weightings in line with the Index, the S&P 500 Index in this case.

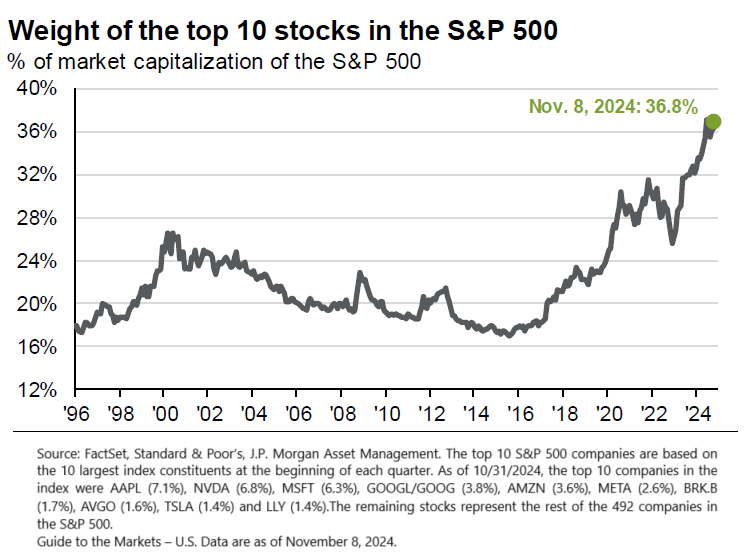

The concentration in the top ten stocks in the S&P 500 Index is seen below. At the end of last week, 36.8% of the S&P 500 Index was invested in just ten stocks. This is the highest concentration level going back to the mid 1990's and surpasses the 2000 technology bubble peak.

Below is a table showing the top ten stocks in the S&P 500 Index along with their respective index weighting.

For investors, concentration risk can cut both ways in regard to one's portfolio return. So long as performance is centered in those handful of stocks, the investor benefits. On the other hand, if performance broadens out, like performance has been doing since the end of the second quarter, concentration is not such a good thing. Additionally, if the concentrated holdings correct after a significant run up, the downside can be significant.

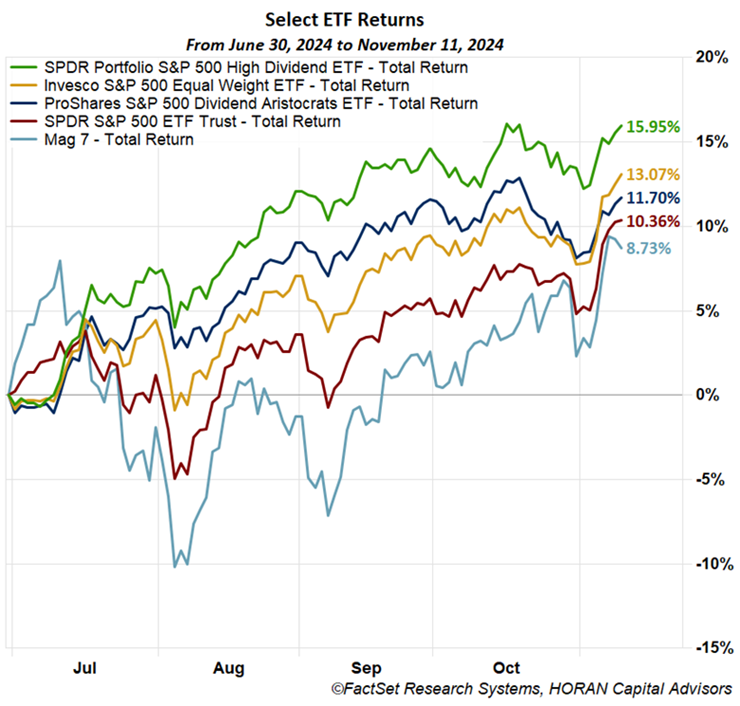

For investor's concerned about concentration risk and its potential consequences, other investment strategies are now generating returns ahead of the S&P 500 Index's return. Below is a chart showing several investment strategies with the dividend focused ones and the Equal Weighted S&P 500 Index (RSP) outperforming both the capitalization weighted S&P 500 Index and the Mag 7 ETF (MAGS) since the end of the second quarter. Reallocating to some of these other strategies may be a reasonable approach to reduce some of the risk associated with the current return concentration of cap weighted indexes like the S&P 50 0Index.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.