Author: David I. Templeton, CFA, Principal and Portfolio Manager

Bonds in one's portfolio can serve as ballast in an equity market pullback. The recent rise in interest rates improves the risk/reward profile of bonds.

Over the long run stocks outperform bonds; however, as an investor approaches retirement age, or near a time when they will rely more heavily on their portfolio for income, they tend to allocate investments towards less volatile asset classes like bonds. Volatility is the other side of the coin to return and represents part of the risk with investments. Investments with lower expected risk, as with bonds, will generate returns that mostly lag higher risk assets, over time.

The recent experience for investors has challenged this understanding though. As recently as 2022 at the end of the year, nearly every asset class generated a negative return. For investors the bond allocation in their portfolio did not provide the risk mitigation that was anticipation and resulted in a balanced portfolio generating one of its worse returns on record. In an article from a few years ago on VettaFi, it is noted,

"Bond losses in 2022 were historic. US Treasury bonds had their worst year since the birth of the nation. 20-Year US government bonds lost -29%, and 10-Year US lost over -12%...Even typically low volatility short Treasurys and mortgage-backed securities lost -4% and -12%, respectively. International bonds performed just as poorly. The Global Aggregate Bond Index had its worst year since its inception and UK bonds had their worst returns in 400 years."

Fed Rate Increases a Headwind for Bonds

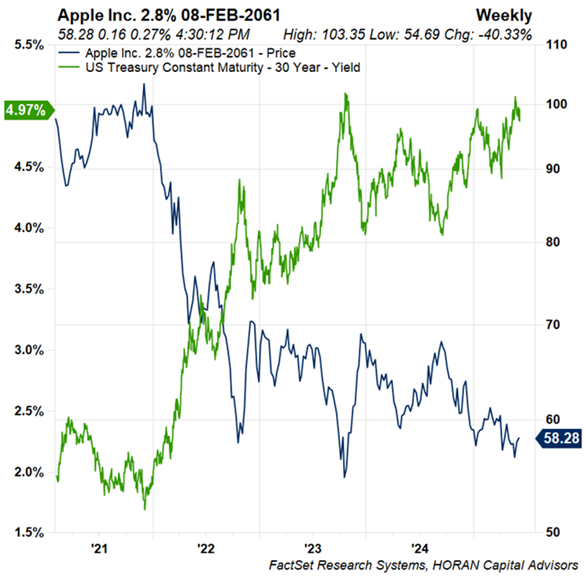

A significant factor that pushed bond prices down in 2022 was the pace of the Fed's interest rate increases in that year. The Fed increased rates seven times from .25% to 4.50%. Interest rates were near zero from early 2020, the beginning of Covid, through the Fed's first increase in April 2022. This near zero interest rate period followed the near zero interest rate period following the Great Financial Crisis in 2008/2009 that lasted from 2008 to the end of 2015. This near zero rate period enabled companies, municipalities and to a lesser extent the government to issue longer maturing bonds at low interest rates. Since bond prices move inversely to the direction of interest rates, this rapid increase in rates contributed to the headwind in bond returns. The other factor that resulted in significantly negative bond returns is the fact many bonds had been issued with a low coupon rate of interest that was paid to investors. In other words, bonds had a low level of support from the bond interest payments to make up for the decline in price. An example of the damage already impacting low yielding bonds issued after the Covid crisis is Apple's (AAPL) 2.8% 2061 maturing bond issued February 8, 2021. At the time of issuance, the bond's price was near par ($100) but now trades at 58 cents on the dollar. The price decline is mostly due to the increase in long term interest rates with the 30-Year U.S. Treasury yield increasing from 1.94% to 4.97% today. This particular bond has a duration of approximately 17.5 years.

Duration is an Important Measure

Trying not to be too technical, but a bond's sensitivity to interest rate changes is measured by a variable known as duration. Duration is measured in years and indicates by how much a bond's price will change for every one percentage point change in interest rates. As an example, a 5-year bond with a yield to maturity and coupon of 3.5% would have a duration of about 4.5 years. With a duration of 4.5, the bond’s price should fall 4.5% for every one percentage point rise in yields, and vice versa. The longer a bond has until its maturity date, typically the longer its duration; thus, indicating a greater sensitivity to changing yields. Also, for identical bonds except for different yields, the bond with the lower yield will have a longer duration.

Looking back at 2022 with the Federal Reserve increasing interest rates four full percentage points, the downward pressure on the above noted bond would equate to an 18% decline in price assuming all interest rates along the maturity spectrum increased by the same amount, which is unlikely. At the five-year maturity, treasury interest rates actually increased about 2.25 percentage points from the beginning of 2022 to the end of that year so the above bond's price would decline by about 10%.

The Bond Impact with Recent Interest Rate Increases

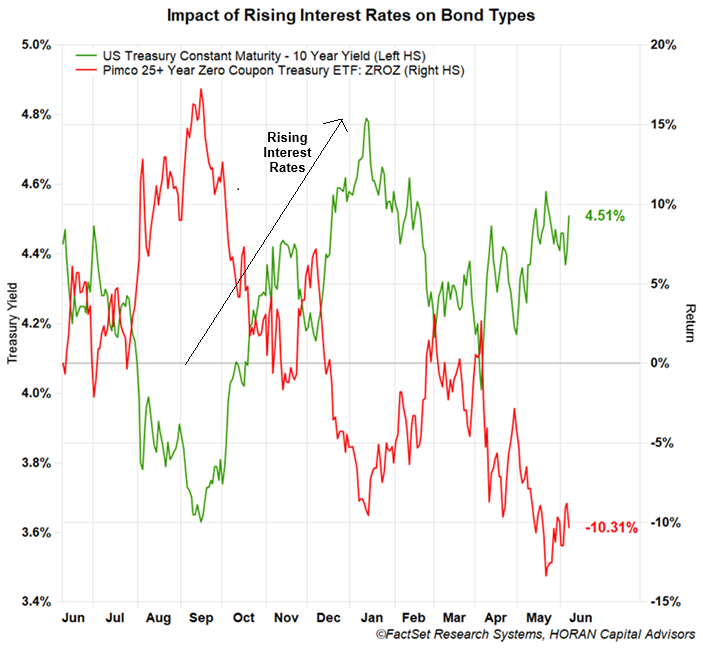

Below are two charts showing the price movement over the last twelve months of the iShares Core U.S. Aggregate Bond ETF (AGG) that trades with a duration of about 5.8 Years and an average yield to maturity of 4.7% and the second chart of the PIMCO 25+ year Zero Coupon U.S. Treasury Index ETF (ZROZ) that has a duration of approximately 27.5 years. With ZROZ investing in treasury investments that do not have a coupon interest payment, i.e., no income yield, the duration of a zero coupon bond is the time remaining to the bond's maturity.

With Higher Yields, Bonds Seem More Attractive as Investments

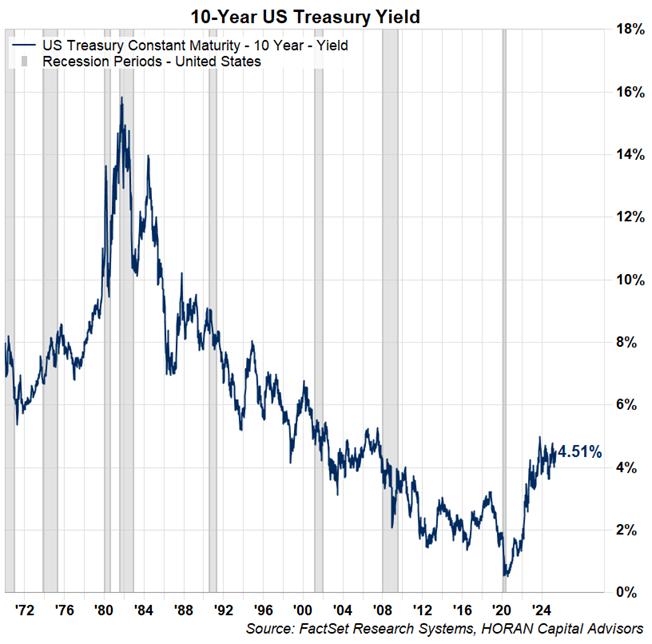

Over the last year the 10-Year Treasury yield has increased from 3.6% in September to 4.51% today. This move in interest rates has negatively impacted the return of lower yielding and long maturity bonds as seen with the return of ZROZ over the last 12-months. A core bond investment like AGG has held up reasonably well though. Interest rates could move much higher if history is any guide. Back in the early 1980's the 10-Year Treasury reached a yield of 15.6% in late 1981. However, it is hard to see rates reaching that level as events, especially inflation, that was a part of the environment then are not in place today.

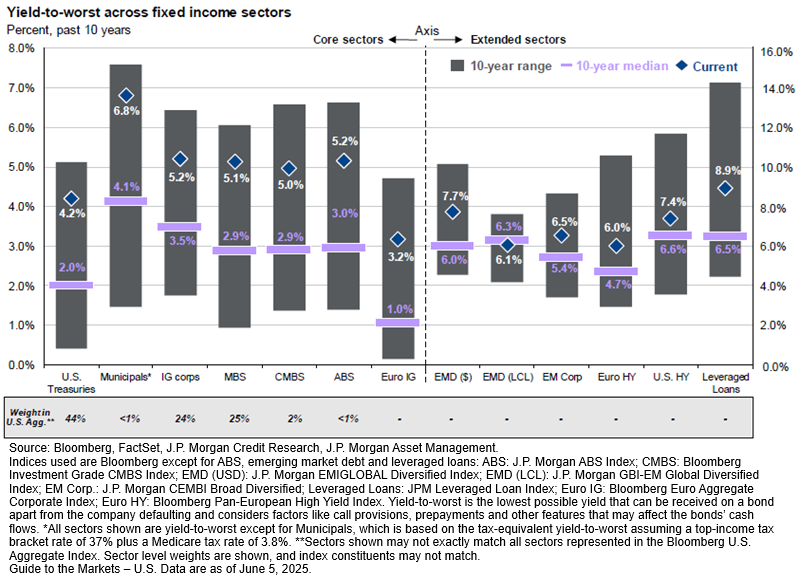

With yields higher today than the recent zero interest rate periods, the risk reward of bonds is more attractive for investors. The below table details various bond categories available to investors. Just focusing on the left half of the table, the blue diamond represents where bond yields are currently with the grey shaded bar representing the range for yields over the last ten years. In most cases on the left the diamonds or yields are in the top quartile of yields over that time period. For the municipal yield of 6.8%, this is the tax-equivalent yield assuming the top U.S. income bracket of 37% and the Medicare tax of 3.8%.

At HORAN Wealth our clients know our bond strategy has been ultra short, short term to intermediate term focused. When interest rates were near zero, we believed bond investors were not adequately compensated for the risk should yields increase and that did in fact play out. Over the course of the last 12-months or so we have reduced the ultra-short exposure and balanced the exposure with short term and intermediate term bond investments. And with rates being higher today, incorporating more bond exposure might serve as ballast in one's investment portfolio when stocks pullback next time.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.