Author: David I. Templeton, CFA, Principal and Portfolio Manager

In the U.S. the consumer segment of the economy accounts for approximately 70% of economic activity or GDP. As a result it is important to evaluate how the consumer is doing and the events that may impact consumer activity going forward.

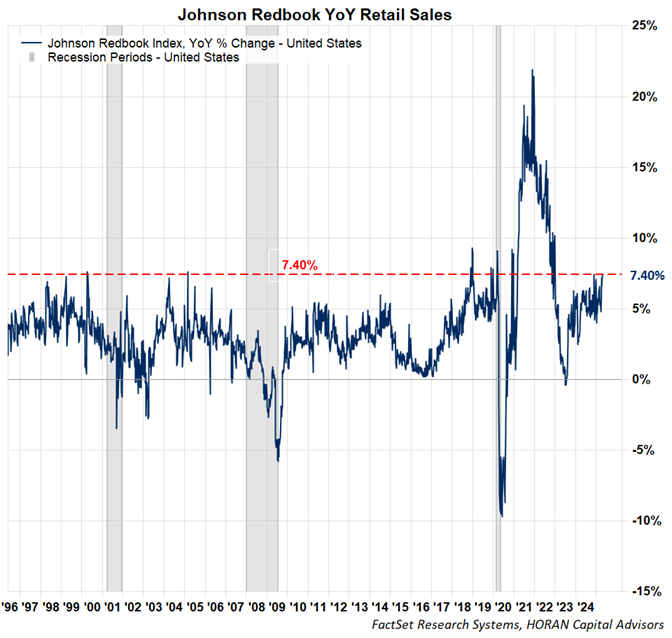

From a broad spending perspective, it does appear the consumer is continuing to spend. The most recent weekly retail sales report by Johnson Redbook shows retail sales increased at a 7.4% year over year rate as of the April 18 report. According to Johnson the Redbook Index represents "over 80% of the equivalent 'official' retail sales series collected and published by the US Department of Commerce." Clearly, retail sales have not fallen off a cliff, yet there is potential the tariff headwinds might impact available products on retailer shelves.

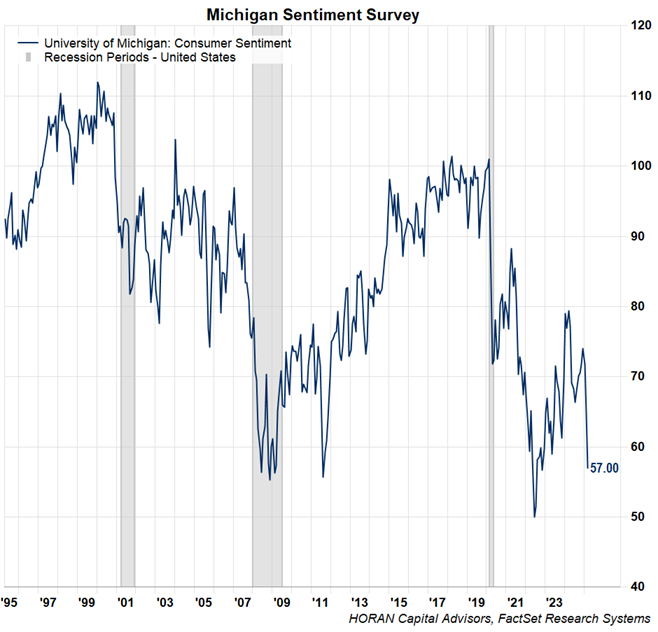

The fact actual activity is showing consumers are continuing to spend is running counter to what consumers are expressing in surveys, i.e., soft data. Below is a chart of the University of Michigan Sentiment Survey and it shows a sharp decline in the March reading. Interestingly, this has yet to show up in the actual hard data, i.e., spending.

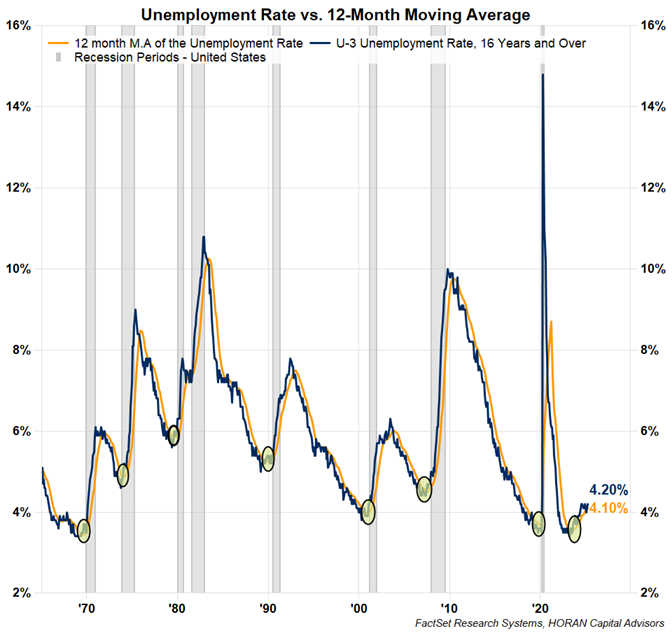

One area beginning to see weakness that directly impacts consumer spending is the state of the job market. The most recent report for employment shows the unemployment rate has moved higher to 4.2%, up from 3.4% two years ago. This has resulted in the unemployment rate moving above its 12-month moving average as seen below. As the circles on the chart show, these crosses tend to occur before recessions. Further insight into the employment market will come in the May 2 release of the Employment Situation Report by the Bureau of Labor Statistics.

One positive is job openings of 7.57 million remain higher than the number of individuals looking for employment, 7.16 million. However, openings are down significantly from levels seen after the Covid shutdown and subsequent reopening. Since September of last year though, job openings appear to have stabilized and actually increased.

It does seem the employment market will continue to experience weakness, especially from the government sector. This weakness is showing up in the Challenger, Gray & Christmas Job Cut Survey. As seen below, the March survey reports over 275,000 job cuts are expected. A majority, 216,915, are in the government sector, certainly a result of the Trump administration's effort to reduce government spending.

Lastly, some areas of the employment market are likely to remain challenged, especially the government sector. For those forced into the job hunt, opportunities are available in the private sector and keeping an open mind about opportunities is important. I recently ran across an interesting LinkedIn post from an individual who moved in a different industry and job position than what she had been doing for the last twenty-five years. Her experience even surprised her.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.