Author: David I. Templeton, CFA, Principal and Portfolio Manager

About a year ago many strategists were calling for a U.S. recession to begin by mid-year this year. A part of the rationale behind this thinking was the pace of the Federal Reserve's interest rate increases which resulted in the yield curve inverting, i.e., short-term interest rates rising above long-term rates. The fast pace and magnitude of the rate increases were thought to significantly constrain employment, constrain business growth due to tightening credit standards, and result in a lull in housing activity due to higher mortgage rates.

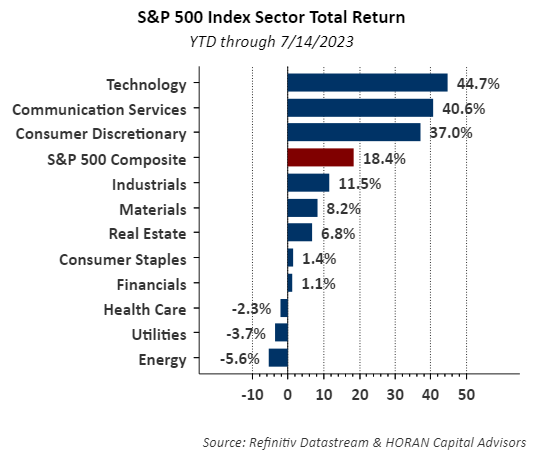

With a little more than half the year behind investors, the S&P 500 Index is up 18.4% on a total return basis. Knowing the equity market and the economy are not necessarily the same, the equity market returns might provide a clue to the future direction of the economy. As the below bar chart shows, economically or cyclically oriented sectors have performed the best this year. Information Technology, Communication Services, Consumer Discretionary and Industrial sectors are the four leading sectors.

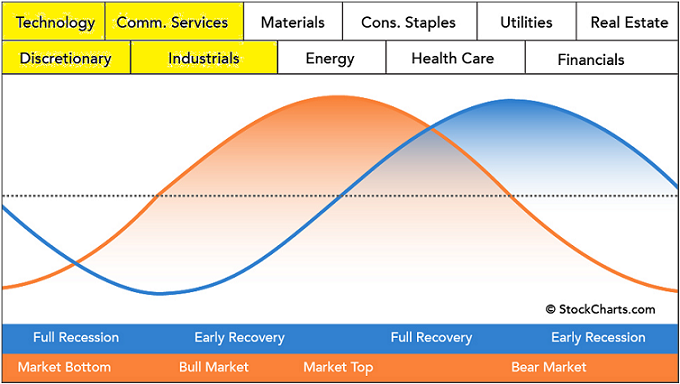

In the next chart, the orange line represents the equity market and the blue line represents the business cycle. Across the top of the chart are the economic stock sectors and the yellow highlight represents the sectors that are outperforming year-to-date as noted above. These are the sectors that perform the best coming out of an equity market bottom, and a market entering a bull market phase. The recovery of these four sectors tend to lead the recovery of the economy, in other words, the equity market is telegraphing a recovering or expanding economic environment. More on this topic is covered in our quarterly investor letter to be published on Monday.

Chart source: stockcharts.com Sector Rotation Analysis

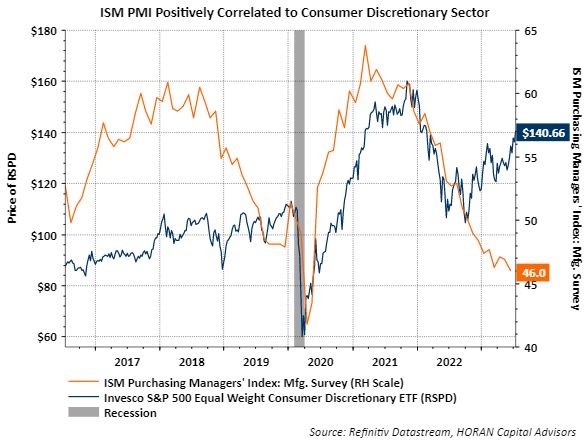

One of the areas of focus recently for strategist anticipating a recession has been the declining ISM Purchasing Managers' Index (PMI) for the manufacturing industry. Readings for this index below 50% are reflective of this part of the economy being in contraction. The current reading is 46%, yet the PMI for the services economy is 53.9%, an expansionary reading. In terms of size, the services sector contribution to the economy is about 75% while manufacturing is just under 15%. Manufacturing is important and becoming more so as more companies move manufacturing back to the U.S. to address supply chain issues that developed during the pandemic. But with services seemingly expanding, it appears manufacturing may turn the corner as well. The below chart shows the Invesco Equal Weighted Consumer Discretionary ETF (RSPD) compared to the ISM PMI for Manufacturing. There is a high correlation to an improving discretionary sector and followed by an improving manufacturing industry. Intuitively this seems to make sense, as consumers spend more on goods and services, manufactures will need to replenish inventories.

As this year unfolded the economic data has been mixed with some data at recessionary levels while other data is indicative of an economy that continues to grow. Much of the difficulty in interpreting the data is a result of the pandemic in my view. Pent up demand continues to be a theme that continues to drive certain segments of the economy, travel and leisure are top of mind. Certainly, the equity market seems in need of a breather given the magnitude of recovery off of the October 2022 low. With the economy possibly set to regain some momentum though, favorable returns seem a likely outcome in the second half of the year, but not higher in a straight line.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.