Author: David I. Templeton, CFA, Principal and Portfolio Manager

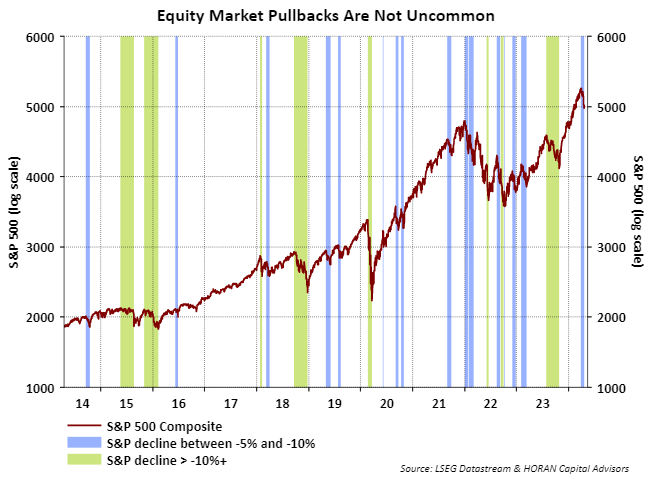

In our March 16, 2024 post we noted, "a near term correction would not be a surprise." This comment was a few weeks early, although the market did not move much higher subsequent to the post but peaked on March 28. Since that time the S&P 500 Index has declined -5.5% through the April 19, 2024 close. The earlier post highlighted the fact the S&P 500 Index had begun to outperform the Nasdaq 100 Index in late January. A rotation of sorts was underway and flows were moving out of the Nasdaq oriented stocks where all Magnificent 7 stocks are represented in the top 10 holdings of the index. Market corrections are a normal function of the equity market as seen below. What has been a bit of a surprise is the uninterrupted advance that occurred since October of last year following the -10.7% correction from July to October.

This rotation seems to be occurring with investors reducing exposure to mega cap stocks. Over the last month the equal weighted S&P 500 Index (RSP) is now outperforming the capitalization weighted S&P 500 Index. On Friday the equal weighted S&P 500 Index actually achieved a small positive gain while the cap weighted S&P 500 Index declined.

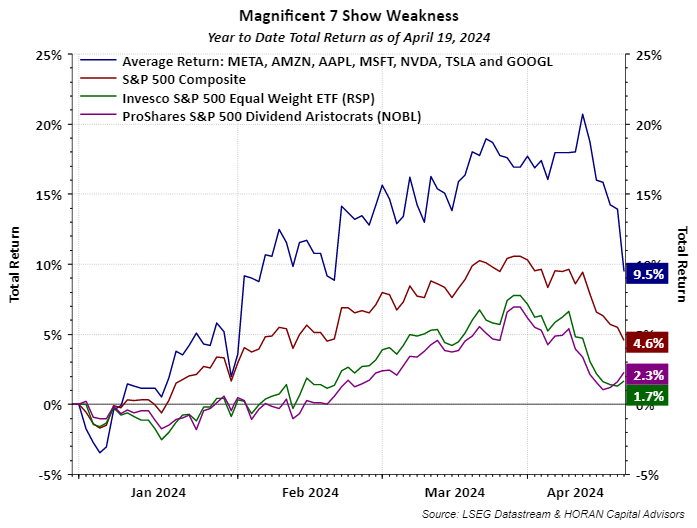

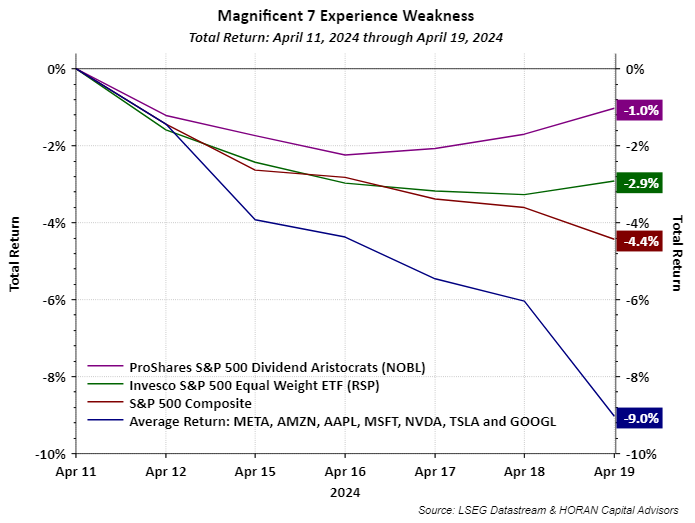

The next two charts provide some detail on the performance of the Magnificent 7 socks. Since the beginning of the year the Mag 7 have outpaced the S&P 500 Index and some of the dividend yielding Indexes. The tail end of the blue Mag 7 line below shows the pullback in these stocks. The second chart shows a shorter time that begins with the peak in the average return of the Mag 7 on April 11, 2024. The Mag 7 average stock return is down -9.0% and far outpacing the -4.4% decline in the S&P 500 Index itself.

Lastly, the market does seem short term oversold as seen in the below chart. This does not mean a bounce occurs and the market is off to the races. Further weakness might take place; however, some stocks that have not fully participated in the market's climb from October last year, might provide an attractive entry point, e.g., higher quality dividend payers, up just 2.3% this year.

Important near term is the fact earnings seasons is in full swing. Company outlooks will be an important indication of the views on the year ahead and company views on the economic outlook ahead. According to LSEG I/B/E/S 70 companies have reported earnings through April 19 with 78.6% reporting earnings above expectations. In a typical quarter LSEG notes 67% beat estimates. Also noteworthy, companies are reporting earnings that are 10.1% above estimates. It is early in the first quarter reporting season, but this is a favorable metric.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.