Author: David I. Templeton, CFA, Principal and Portfolio Manager

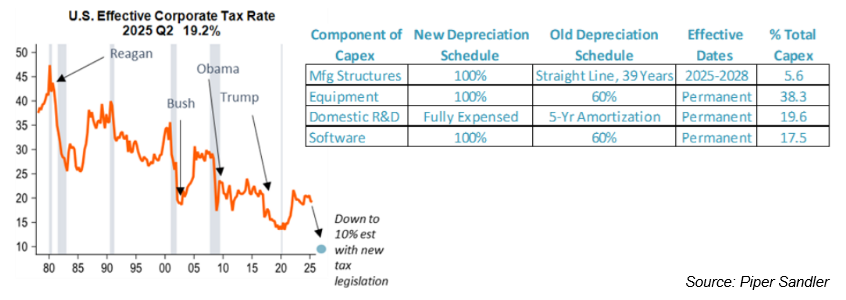

As it relates to the outlook for 2026 it is often said the stock market and the economy are not the same. One reason for this is the fact certain areas of the stock market do well under different economic environments. Nonetheless, we are cautiously optimistic about the economy going into 2026. Some of the recent weakness, especially around the employment market, seems to be an after effect from the recent government shutdown. As the calendar nears turning to the new year, the economy is likely to benefit from the stimulus resulting from the passage of the One Big Beautiful Bill Act (OBBBA). With passage of the OBBBA the effective U.S. Corporate Tax Rate will fall to near 10%, providing a boost to manufacturing as seen below.

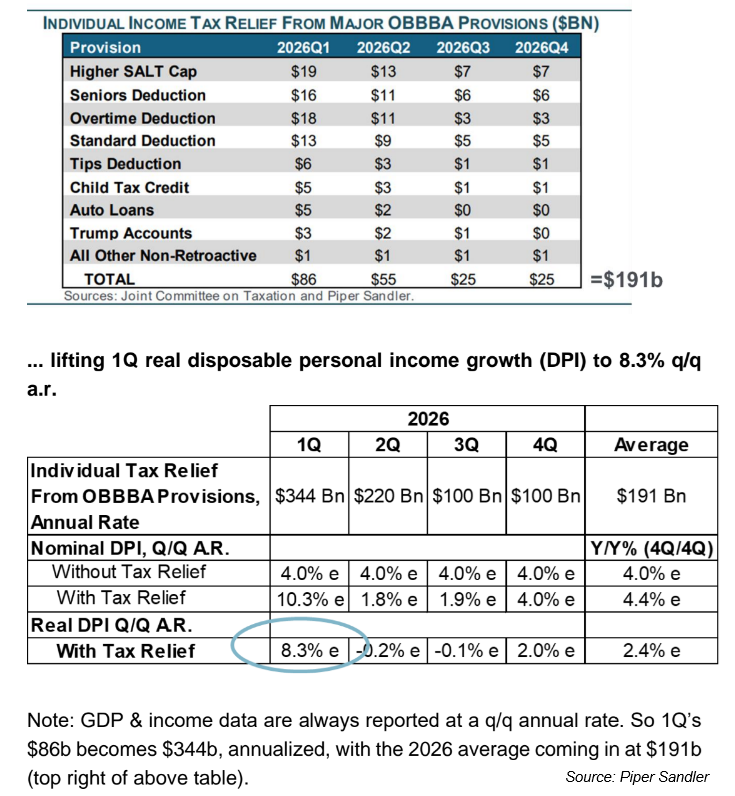

Additionally, large tax refunds may be enjoyed by some taxpayers due to the OBBBA’s tax relief pertaining to certain parts of the tax code as seen in the below table. Real consumer spending is increasing in spite of the shutdown, and some taxpayers will receive a benefit with some provisions of the OBBBA, i.e., no tax on tips, higher SALT tax deduction, etc. As detailed in the below tables, the cuts could provide stimulus up to $191 billion and increase first quarter real disposable personal income growth to 8.3% QoQ.

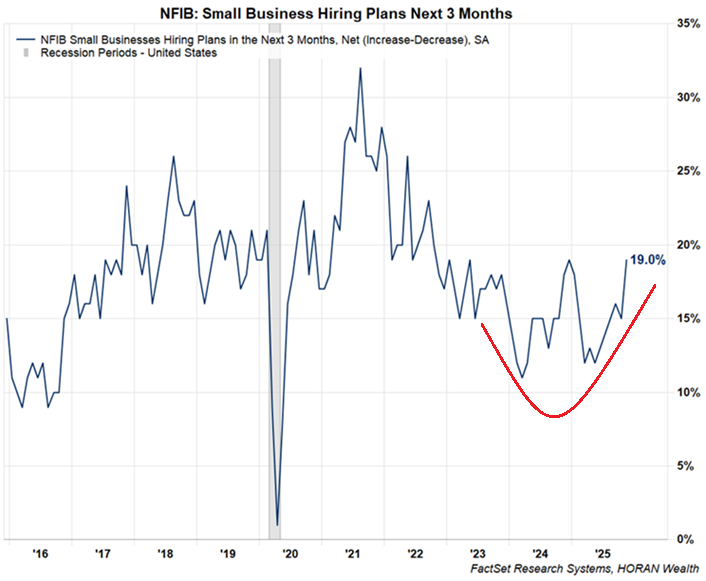

Last week, the National Federation of Small Businesses (NFIB) released its monthly Economic Trends report that surveys small businesses and one important area noted was the improvement in small businesses that intend to increase hiring. This variable tends to lead the unemployment rate by 6 months so potentially lower unemployment ahead too.

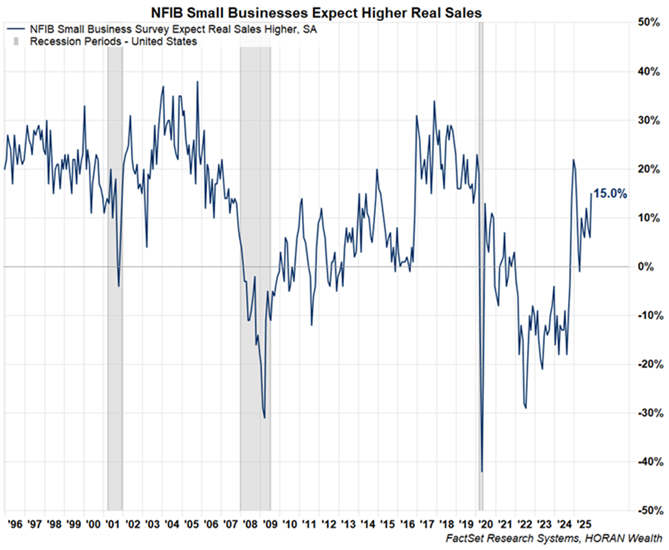

Additionally, with real disposable income expected to see near double digit growth in the first quarter, this will be on top of what small businesses currently expect around sales growth. As seen in the below chart the NFIB November Survey shows a steady improvement in businesses expecting higher sales. The 15% figure is near levels seen coming out of prior recessions.

I will not write to much on the necessity for a more accommodating monetary policy by the Fed but only say with an economy that seems to be improving and OBBBA tax relief stimulus in the first half of 2026, a more dovish Fed might not be necessary. Assuming the stock market does not fall out of bed in the remaining few weeks of December, the S&P 500 would generate a nearly 20% annualized return over the last 3-years. The long-term average return on the S&P 500 is closer to 10% so we’ve been running above that trend for several years now.

While we are cautiously optimistic for all the reasons stated above, a little breather would not be a surprise. In other words, maybe the market is a little choppier in 2026 than this year, not counting the March/April tariff induced pullback. The above table is sorted on the 3-year return column and shows the strength across the various asset classes the last 3 years.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.