Author: David I. Templeton, CFA, Principal and Portfolio Manager

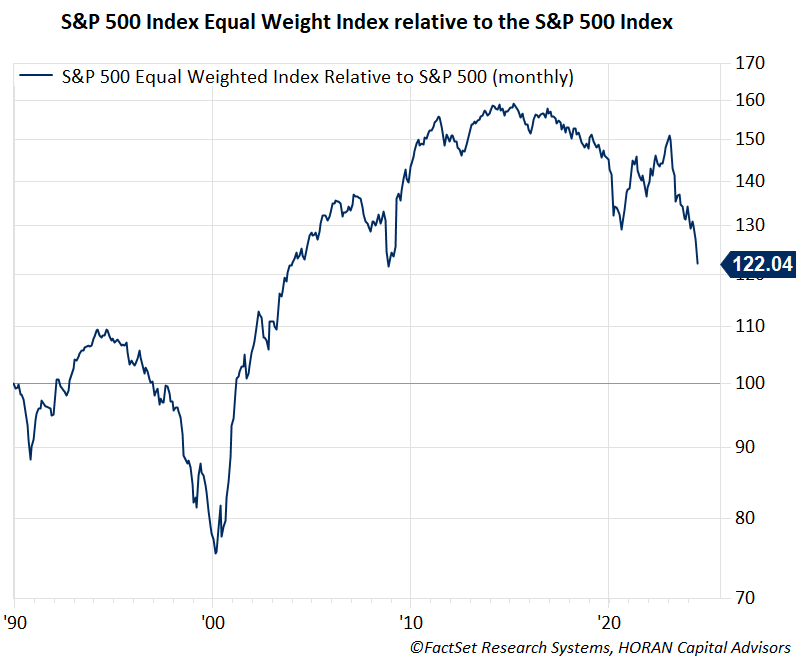

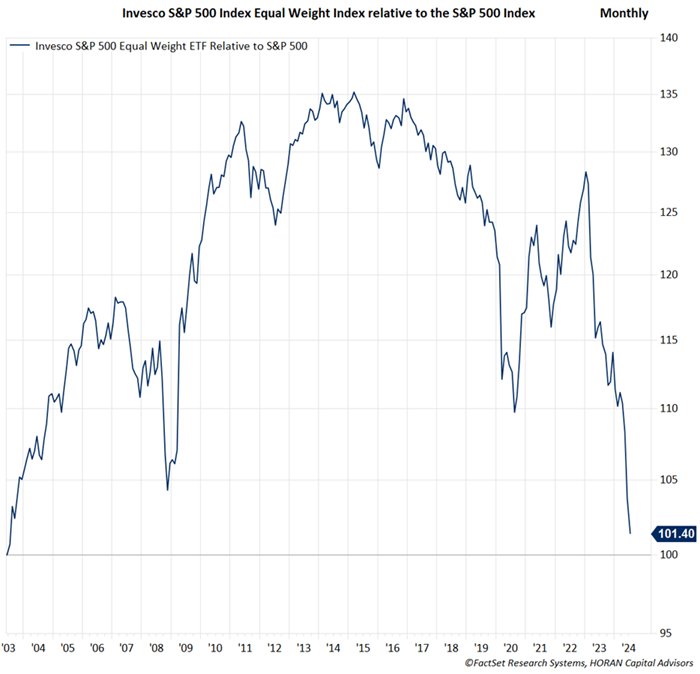

In evaluating the recent investment market and economic data, it is notable the amount of the data that is providing conflicting signals. One equity market factor that currently stands out is the seemingly narrowness of the market. S&P Dow Jones Indices has noted in their prior research work that narrowness itself, or lack of market breadth, is not uncommon. What is notable today is the magnitude of the difference in return between some of the various indices. For example, since S&P launched the S&P 500 Equal Weight Index back in 2003, with back-tested data to 1970, this index has outperformed the cap weighted S&P 500 Index as seen in the below chart.

Since the index launch in 2003 though, most of the outperformance has been erased by the S&P 500 cap weighted index outperformance since the beginning of 2023.

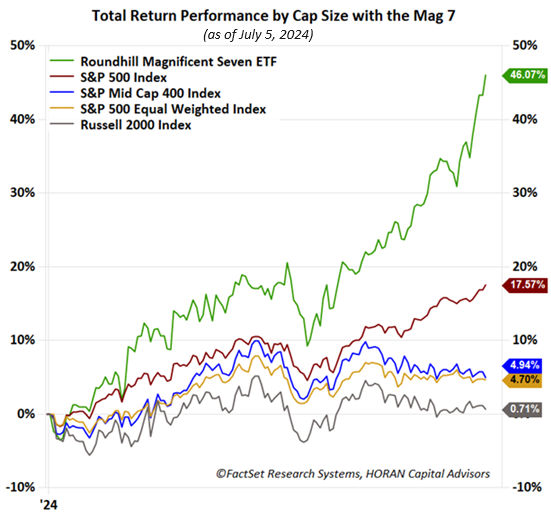

In a May Wall Street Journal article, it was noted at that time the difference in the year-to-date return between the cap weighted and equal weighted S&P 500 Index was the widest on record. Even the other capitalization indexes are lagging the mega cap stocks. As the below chart shows on a year to date basis the S&P Midcap 400 Index is up just 4.94% as of July 5, 2024 and the Russell 2000 Index of small company stocks is up only .71%. One of the best performing Indexes is the one that tracks the Magnificent Seven stocks, the Roundhill Magnificent Seven ETF (MAGS), and it is up 46% so far this year.

With a stock market that has shown narrow breadth like the current one, downside volatility may be lessened as fewer stocks have participated in the rally to the extent the mega caps have, specifically the Mag 7 stocks. Jim Paulsen, a former Wall Street Economist and Chief Investment Strategist, noted in a recent article, "In the contemporary Bull market, however, concentration has been so intense, most stocks have not participated excessively making the Bear’s job much more difficult. Without broad economic or stock market vulnerabilities, an “imminent” Recession or Bear market may remain elusive." His article, Has S&P 500 Concentration Actually Reduced Stock Market Vulnerability, is a worthwhile read.

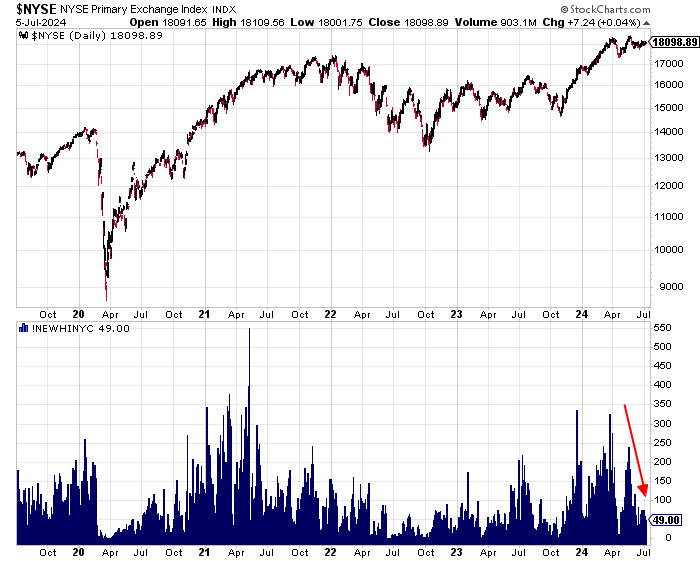

During bull markets it is common for an increasing number of stocks to reach new highs; however, of late though this has not been the case. The bottom panel in the below chart shows the number of New York Stock Exchange (NYSE) stocks that reach a new high on a given day. On Friday only 49 NYSE stocks out of about 2,400 reached a new high. With the S&P 500 Index up over 35% since the October 2023 low, one would expect more stocks to be reaching new highs.

One factor contributing to the equal weighted S&P 500 Index outperforming over the long run is the fact a larger number of stocks contribute to the return. These other stocks are the smaller ones within the index. For a healthy market it is beneficial for some of the other equity asset classes to begin contributing to the favorable return environment, like stronger performance out of the small and mid-cap stocks. It seems plausible that a large correction is not a certainty given the narrow participation, but the weaker returning stocks might begin to gain ground while the mega caps trade sideways. Certainly, the mega caps could correct, but maybe the asset classes that have not gained much ground since the year began will serve as the port in a potential market storm.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.