Author: David I. Templeton, CFA, Principal and Portfolio Manager

Knowing the economy and investment market are not one and the same, and can function out of sync at times, possibly the current environment is such they are actually in sync. That is, the equity market is trending higher on the back of an economy that is growing, but not growing at an exceedingly robust or inflationary pace. An article appearing in a late February Barron's weekly newspaper, What Everyone Got Wrong About the Economy—and the Ominous Implications for the Fed ($$), highlights the difficulty forecasters have had predicting the direction of the economy and market. Of course, much of the difficulty is attributable to the aftereffects of the pandemic and the economic shutdown of the global economy. On top of this, the monetary and fiscal stimulus pushed out to consumers and businesses is still finding its way into the economy. In short, the Fed is having a difficult time delivering on its 2% inflation target as the economy continues to trend higher.

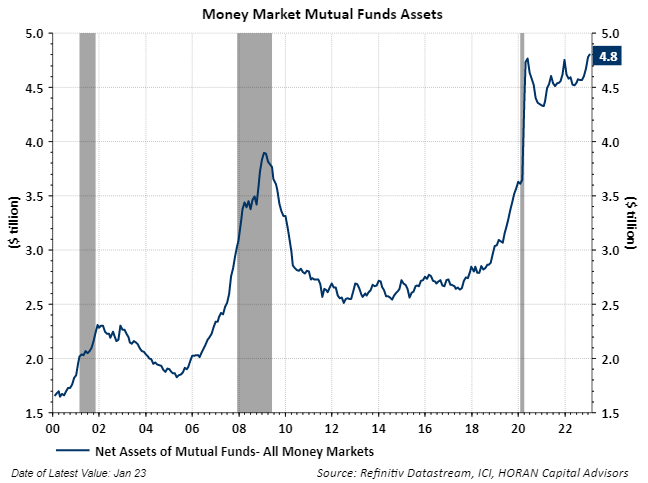

The amount of cash that remains on the sidelines is near a record high at $4.8 trillion. As the Federal Reserve increases interest rates, and as money market interest rates follow higher too, the increase in interest payments on this savings is significant. One year ago money market interest rates were near zero percent compared to today's rate of over 4.5%. This incremental increase in interest earnings, $216 billion, serves as stimulus the owners of the savings accounts can spend. The implication for the Fed is higher interest rates are serving as stimulus for the economy and not what the Fed's intention is as they attempt to tighten monetary policy.

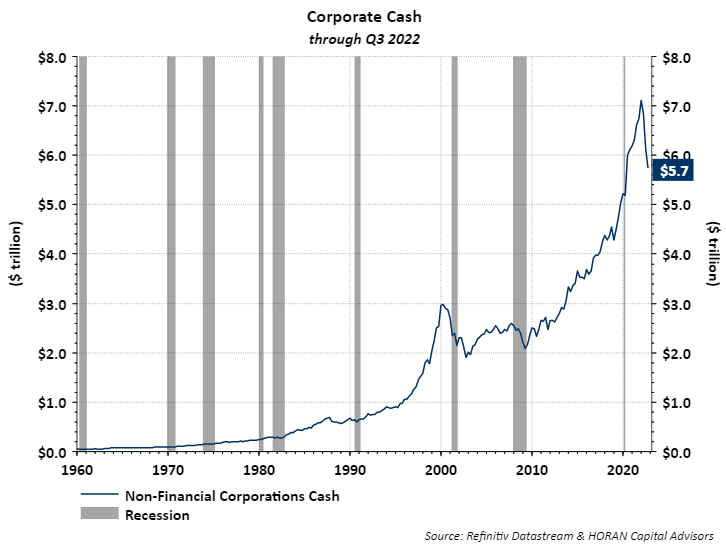

Similarly, corporate cash remains at a high level at $5.7 trillion. Historically, higher interest rates constrain bank lending to companies; thus, slowing economic activity. In part, due to the government stimulus programs, companies remain flush with cash.

One such stimulus program passed by Congress as recently as mid-year 2022, the $280 billion CHIPS and Science Act, includes support for semiconductor manufacturing in the U.S. These are funds that bypass the impact of a tighter monetary policy pursued by the Fed and continue to serve as stimulus for the economy.

From an economic perspective some of the data is indicating economic activity remains strong. In Friday's Investor's Business Daily a brief economic summary was provided with the lead-in titled, Economic Data Strong, and noted,

"Initial reads on the U.S. economy in February show growth may have remained too hot after a sizzling January. The Institute for Supply Management's service-sector activity index dipped just one-tenth of a point, less than expected, to 55.1, far above the neutral 50 level. The current business index, which had jumped 6.9 points in January amid unusually warm weather, gave back 4.1 points but remained robust at 56.3. The factory sector remains in the doldrums. However, the ISM manufacturing index edged up three-tenths of a point to 47.7, still modestly below neutral. New jobless claims dipped 2,000 to 190,000 in the week through Feb. 25, remaining below 200,000 for a seventh week. Unit labor costs were revised significantly higher for Q4."

"China's official manufacturing index jumped to the best level in nearly 11 years, while a services gauge ramped up in February as well. Momentum is building following the end of the "zero-Covid" policy and with China New Year over."

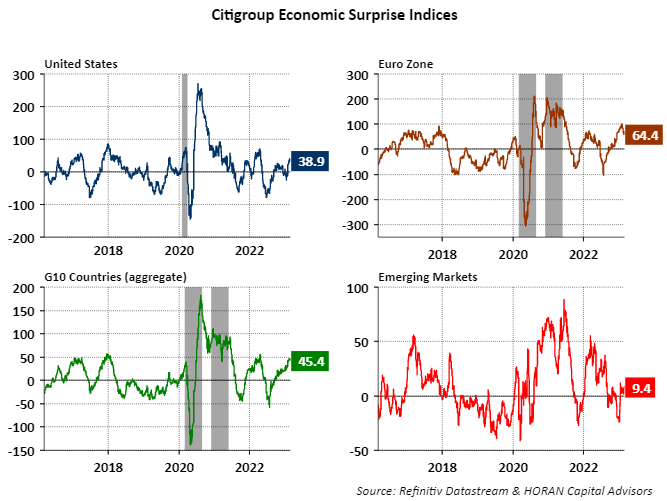

This economic strength is showing up in Citigroup's Economic Surprise Indices. As the below chart shows the economic data is surprising to the upside, not only in the U.S. but internationally as well.

Last week I wrote a post, Equity Market At Important Level Technically, and noted the S&P 500 Index had violated an important upward trending support line. This past week's market advance higher recaptured that support. Now investors want to see upside follow through by the market. Importantly too is the fact another higher low has been created.

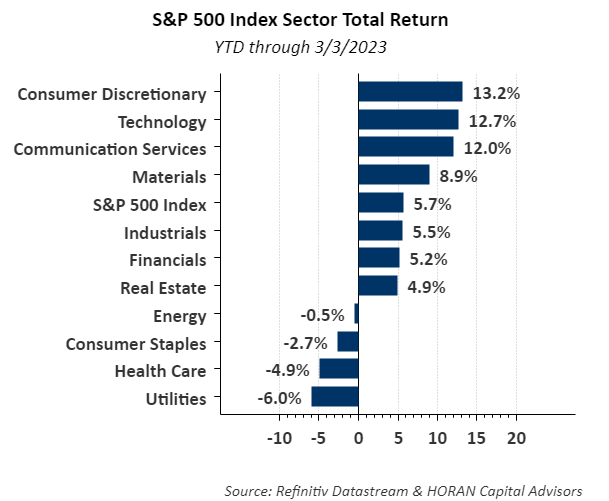

Looking at the S&P 500 sectors, the ones generating the best performance on a year-to-date basis are the economically sensitive ones, Consumer Discretionary, Technology, Communication Services, Materials and Industrials. The lagging sectors are the defensive ones, Utilities, Health Care, Consumer Staples. From an equity market perspective, investors are rewarding the economically sensitive ones over the defensive ones.

As seen in the above chart the S&P 500 Index is up 5.7% on a total return basis this year. Since the low on October 12 of last year the S&P is up over 13%. The market does not move higher in a straight line and the February decline of -2.56% for the S&P 500 Index is a testament to this fact.

Some of the market volatility centers around corporate earnings. The below table shows S&P 500 companies are expected to collectively report a down earnings quarter for the fourth quarter of 2022. The first and second quarters of 2023 are expected to result in a decline in year over year quarterly earnings growth as well. Beginning in the third quarter though, earnings for S&P 500 companies are expected to resume their growth. Stocks tend to trade on forward earnings expectations and this year's favorable equity market returns might be the result of investors looking over the earnings valley of Q2 2023 and looking at expected growth in the second half of this year.

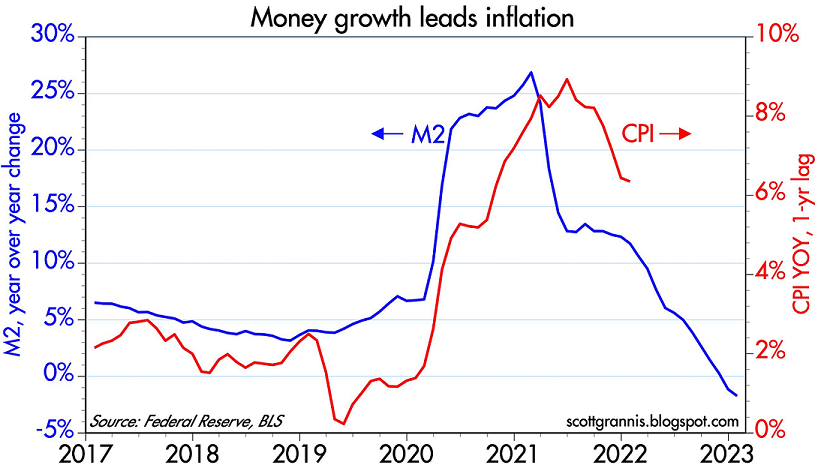

With the elevated level of inflation being experienced today, it is important to note corporate earnings are getting a lift by companies passing through higher cost via higher prices. In some cases companies are reporting lower unit volume at the same time earnings are increasing. In an interesting article I read last week, M2: The Smoking Gun of Inflation, the author notes the reduction in the money supply (M2,) pursued by the Fed should lead to a decline in inflation if history is any guide.

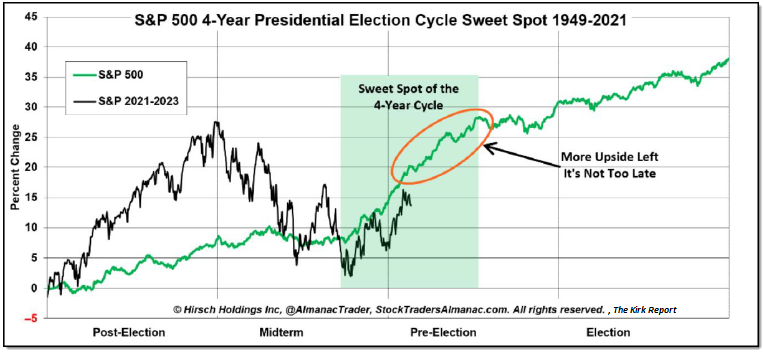

In summary, this is a difficult economic and market environment to forecast. Much of the uncertainty centers around the aftereffects of the pandemic. The S&P 500 has recovered nicely from its October low, yet stocks largely remain below the highs reached in January of 2022 when the S&P 500 Index reached 4,800. However, from a seasonal perspective, the market is in a favorable spot within the 4-Year presidential election cycle as seen below.

Also worth noting is the fact the market has a tendency to be more volatile during periods where the Fed is raising short term interest rates. With the Fed Funds target rate currently 4.75%, this seems about a neutral rate for the economy. In other words, future rate increases by the Fed should not be a surprise. If the decline in M2 as seen in the above chart leads to lower inflation, possibly the Fed is nearer the end of rate hikes and the Fed might actually generate a soft landing for the economy. The mixed economic data of late, though exceeding expectations, might foretell a continued favorable period for the equity market and the economy.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.