Author: Zac Martin, Senior Investment Analyst

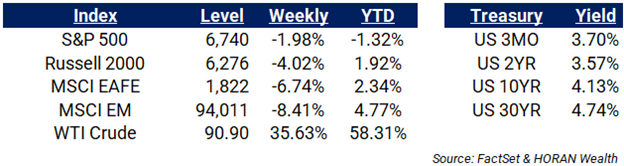

Week Ending March 6th – Back to the Middle

War with Iran: The S&P 500, and other major indexes, have traded lower over the past week due to increased escalation with Iran. Geopolitical concerns have begun to boil over and the news cycle is beginning to shift its concerns to the economic impact. First, and most obvious, is higher oil prices and how that will affect CPI reports as well as FOMC rate decisions. While the near-term impact on oil prices is meaningful, the market is not pricing in a long duration for this increase. Below is the current futures curve for WTI Crude, as the expiration date increases the futures price decreases, implying a near-term bump but normalization lower over the coming year.

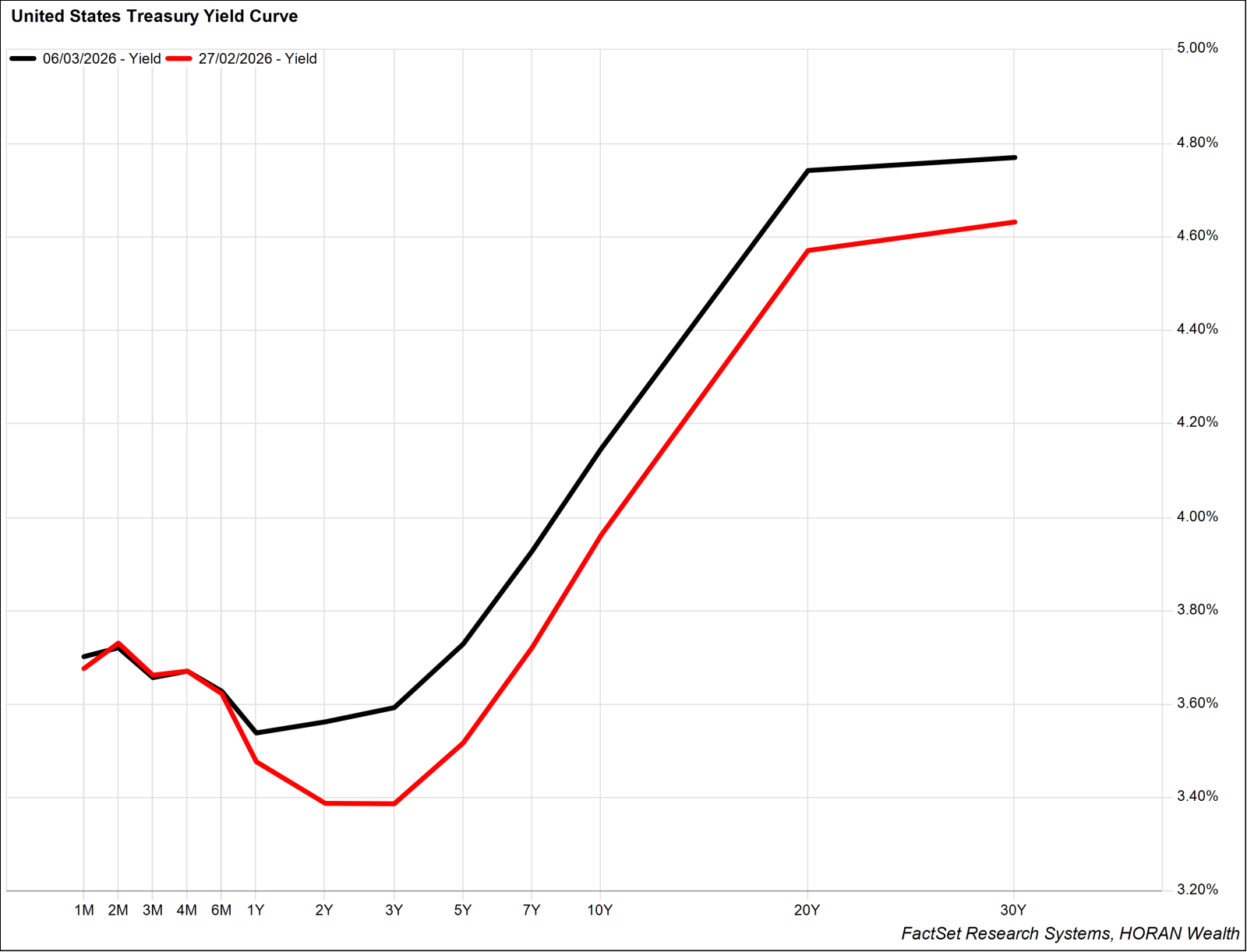

Despite the bump, this could cause CPI to report higher than expected for the next several reporting periods. FOMC rate cut probabilities have moved slightly lower since the initial strikes and US Treasury rates have moved higher. Below highlights last week’s shift in US Treasury yields:

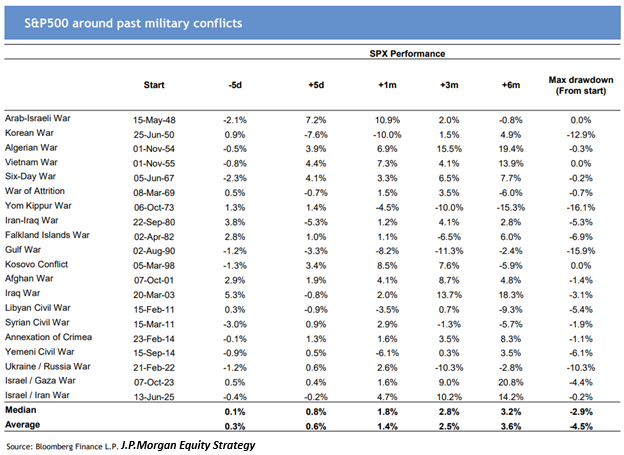

While markets in the near-term have sold off, an analysis of historical conflicts would suggest that markets could rally after an initial drawdown. We have discussed this at length in a recent post. Below is a chart from JPMorgan that highlights this relationship:

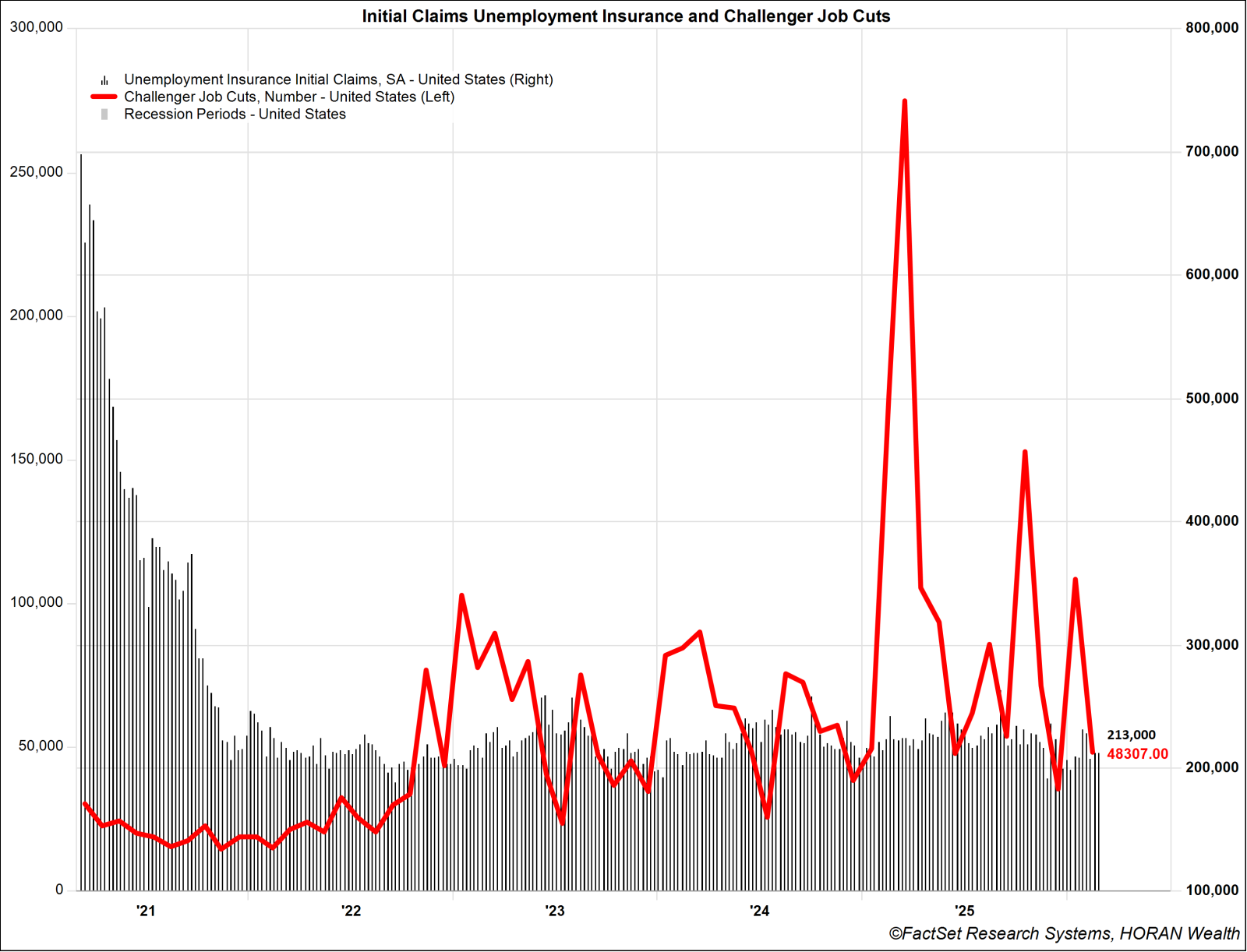

The Employment Situation: Nonfarm payrolls for February fell below the consensus estimates, with payrolls declining by -92K. The decline follows an increase in January of 126K, primarily due to a decrease in health care payrolls as strike activity increased in February. Generally, no sectors faired much better as no sector posted positive payroll growth. Additionally, December’s report was revised down to a decline of -17K from +48K. The Unemployment Rate also ticked up to 4.4% from 4.3%, as the labor market continues to weaken. To be clear this weakness is seemingly from the hiring side as firms continue to delay hiring programs. This becomes more evident as Initial Unemployment Insurance Claims have remained relatively stable. Additionally, Challenger Job Cuts have also been reporting in a more ‘normal’ range, barring DOGE effects from early 2025.

The Week Ahead:

- NFIB Small Business Index (3/10)

- Consumer Price Index (3/11)

- GDP Q4 2025 & Personal Consumption Expenditures (3/13)

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.