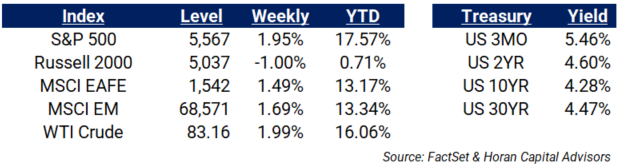

Author: Zac Martin, Investment Associate

Week Ending July 5th – Happy 4th

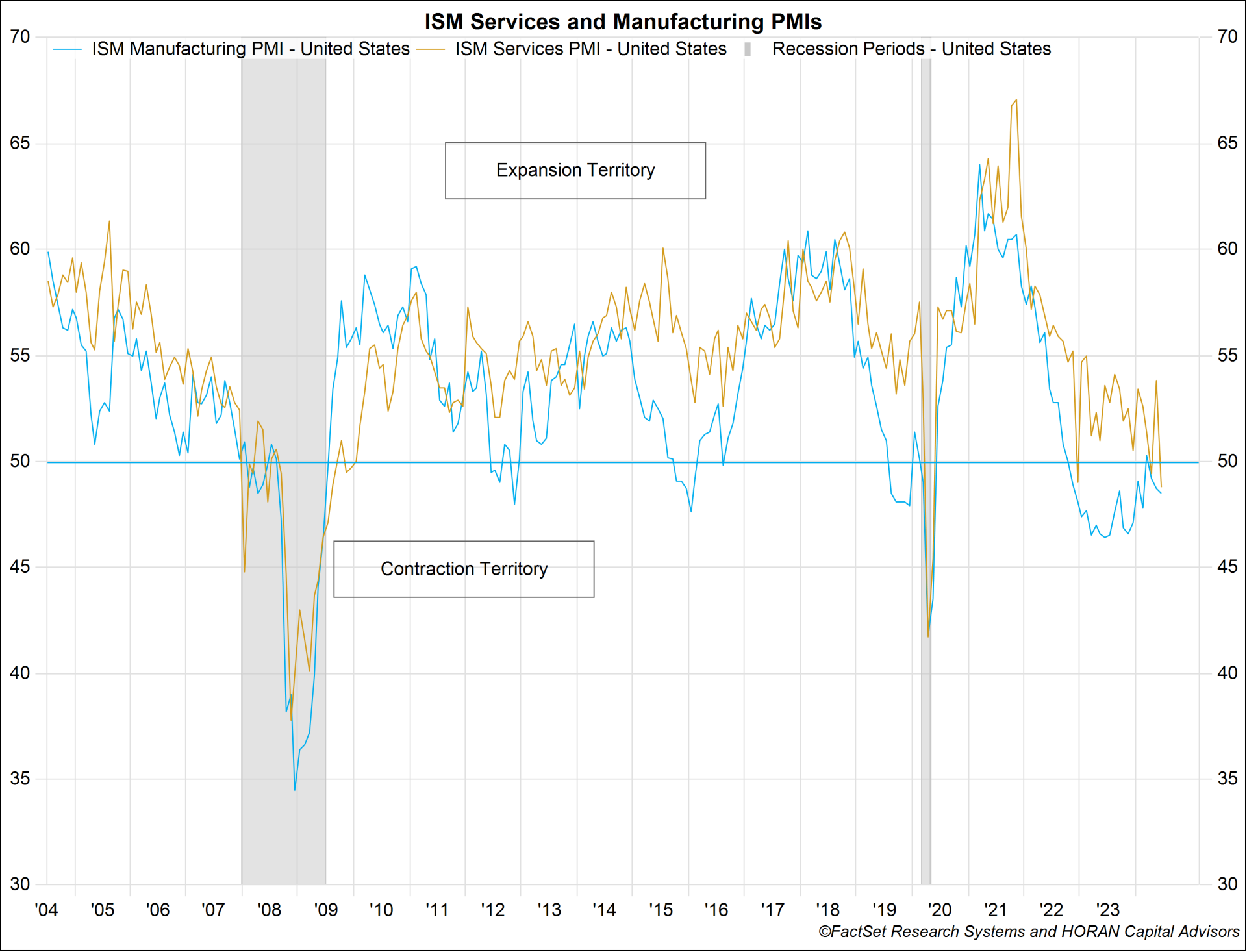

- ISM Manufacturing PMI continues to decline, decreasing by 0.2% to 48.5%. This contraction was led by a new negative trend in employment, production, Imports and New Export Orders. (Chart)

- ISM Services PMI contracted for the second time in the last three months, decreasing by 5% to 48.8%. The services PMI has not reported back-to-back months in contraction since April & May 2020. (Chart)

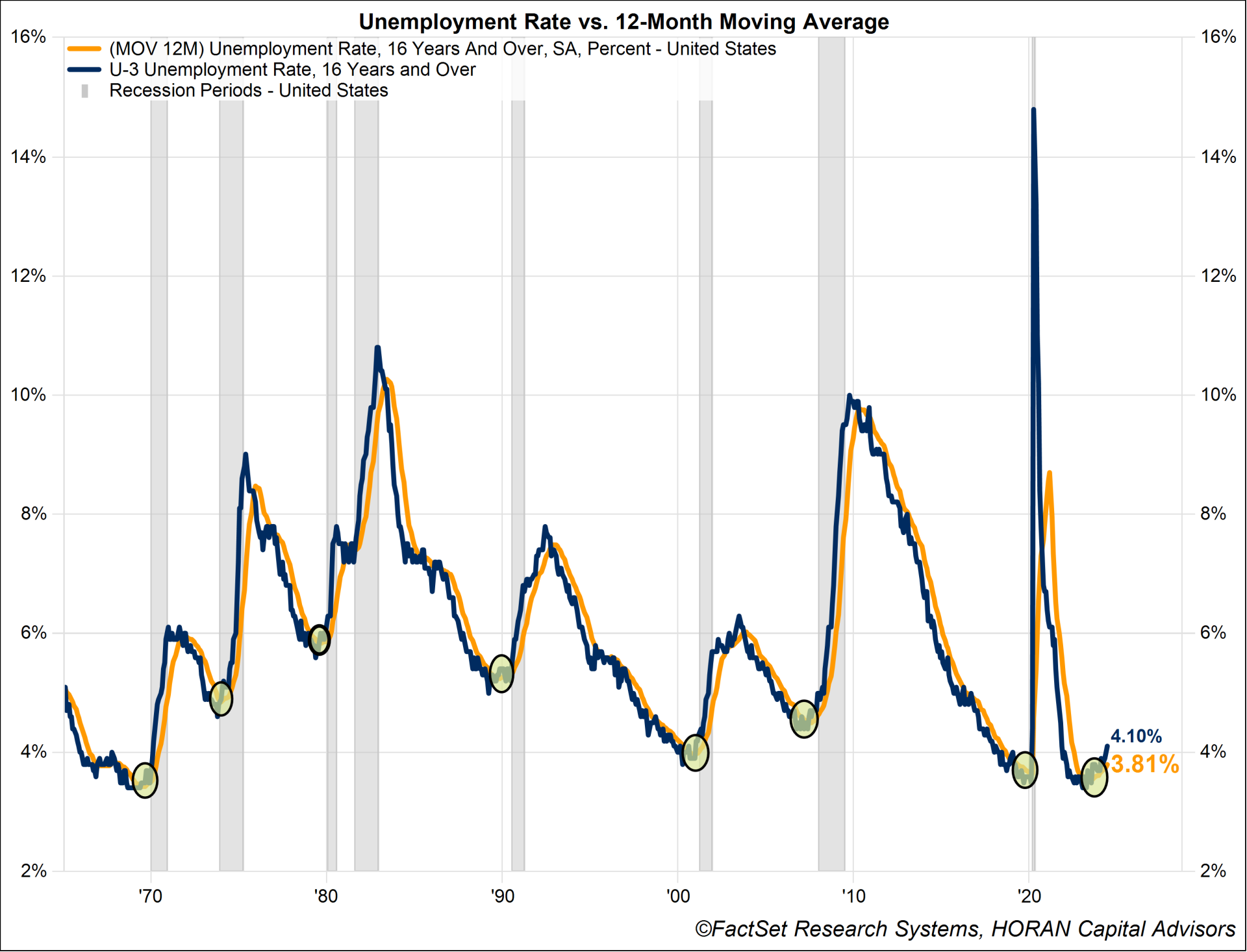

- The Employment Situation for June saw an increase of unemployment to 4.1% up from May’s rate of 4.0%. Meanwhile, nonfarm payrolls increased by 206k, which was led by a 70k increase in Government jobs and a 49k increase in healthcare jobs. (Chart)

- FOMC Minutes for June’s meeting, the economic outlook shifted slightly with the Fed seeing more upside risk to inflation pressures and skewing the forecast for economic activity to the downside. The Fed sees prolonged tightness in financial markets and deteriorating household finances.

{kind=link}

{kind=link}

The week ahead:

NFIB Small Business Index (7/9)

Consumer Price Index (7/11)

Producer Price Index (7/12)

Earnings: JPM, WFC, C, BK, FAST (7/12) – Start of Earnings Season

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.