Author: Zac Martin, Investment Associate

Weeks Ending April 4th and April 11th – Liberated

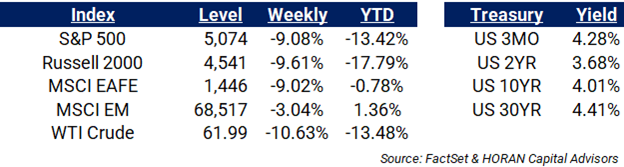

Below, Market Returns for the week ending April 4th:

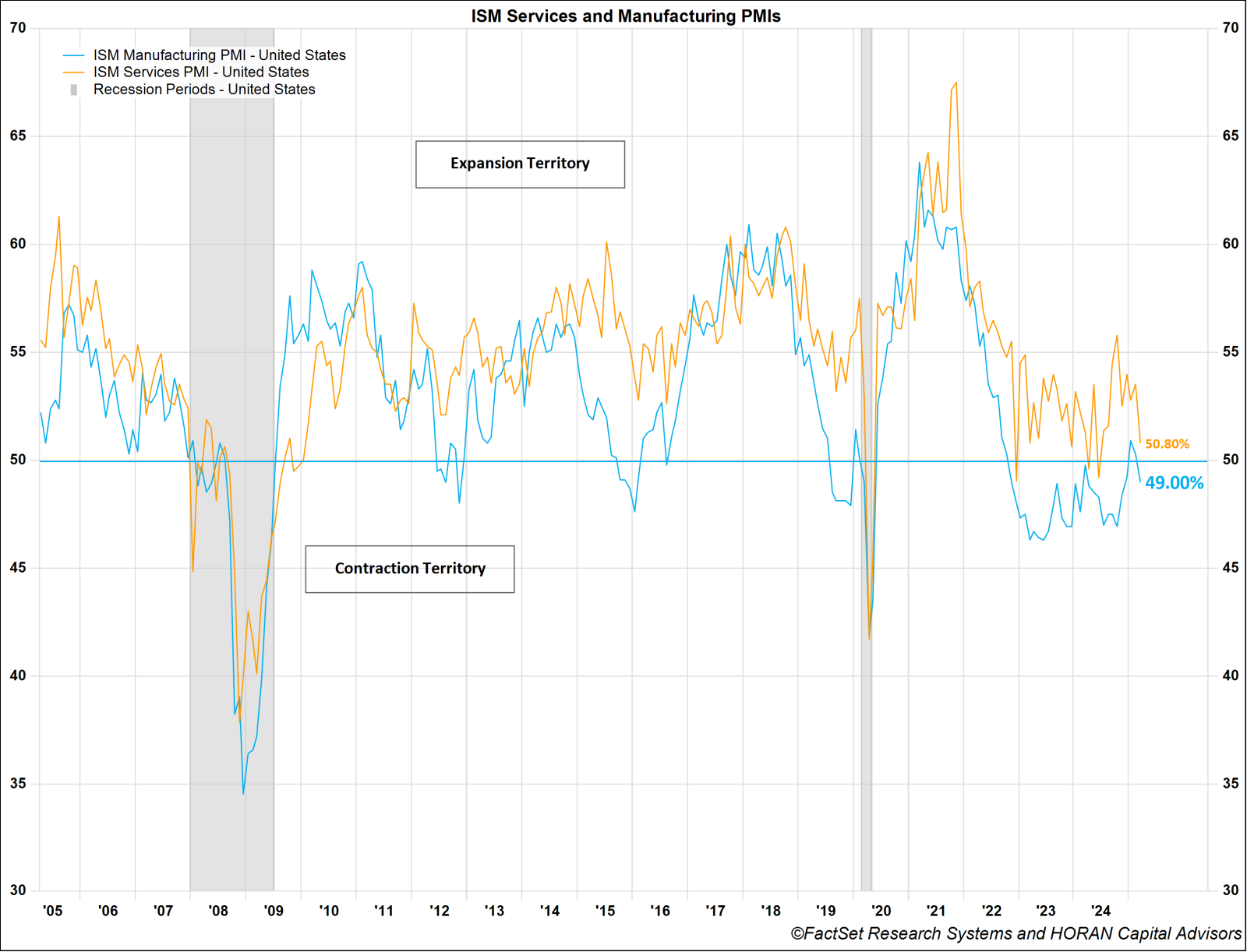

ISM PMIs, both manufacturing and services decreased, manufacturing crossed into contractionary territory while services remain in expansion. New Orders and Backlog remain the largest headwinds for these indicators, while recently sentiment around employment has shifted into a contraction.

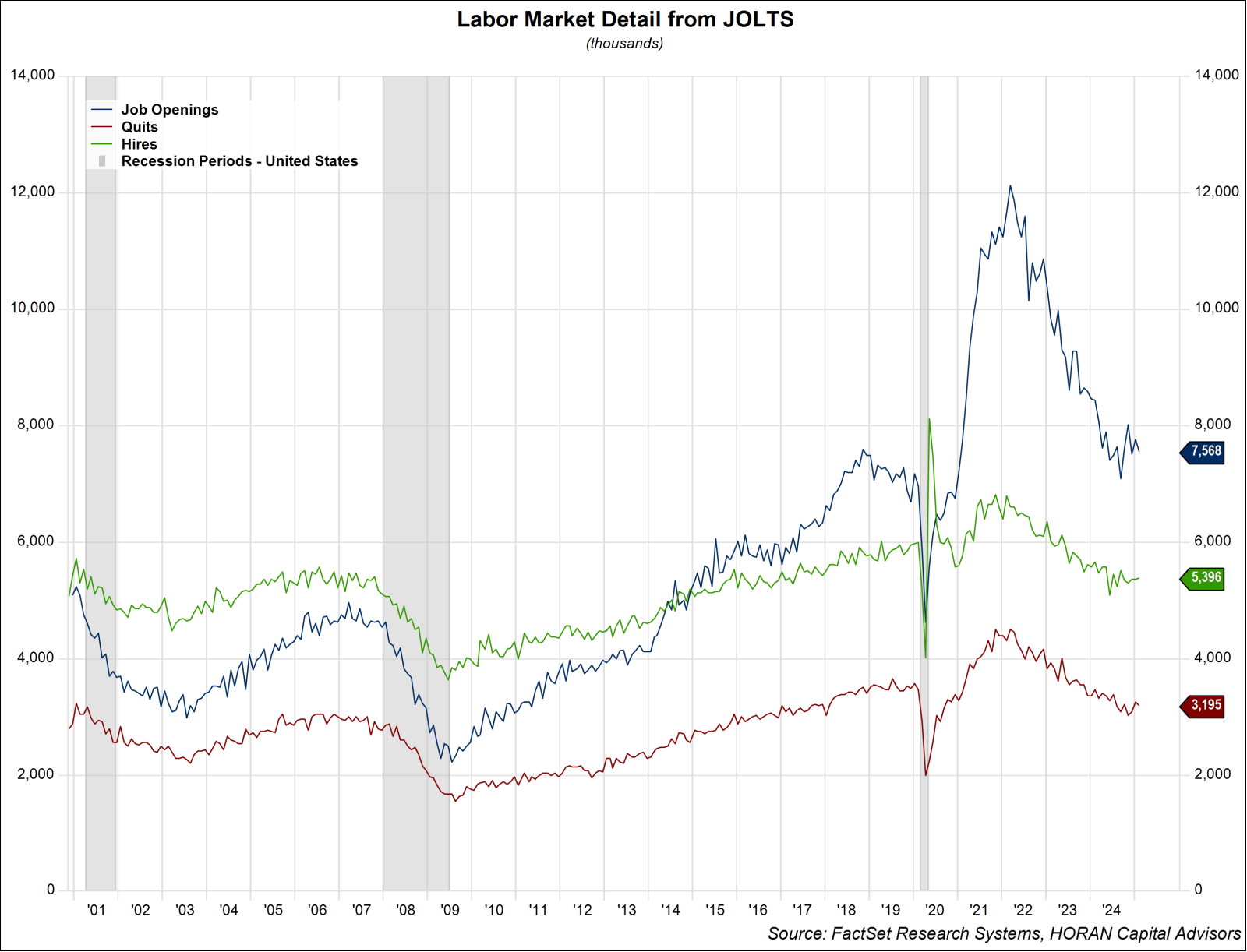

JOLTs report, Job openings continue to decrease while separations remained relatively unchanged. The decline in job openings was a surprise to economists, which expected 7.68Mil versus an actual number of 7.568Mil. Additionally, Nonfarm Payrolls increased by 228,000, government jobs decline by 4k and unemployment increased to 4.2%.

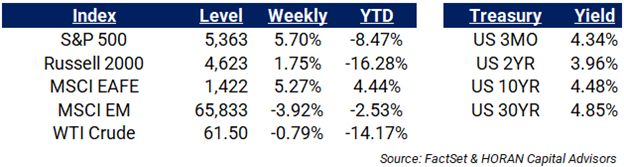

Below, Market Returns for the week ending April 11th:

NFIB Small Business Index declined in March’s report, pessimism continues to weigh on the outlook to find qualified labor to fill job openings. Expectations for the economy to improve and for sales to increase, declined meaningfully. Inversely, plans to make capital outlays over the next six months increased, primarily being spent on new equipment and vehicles.

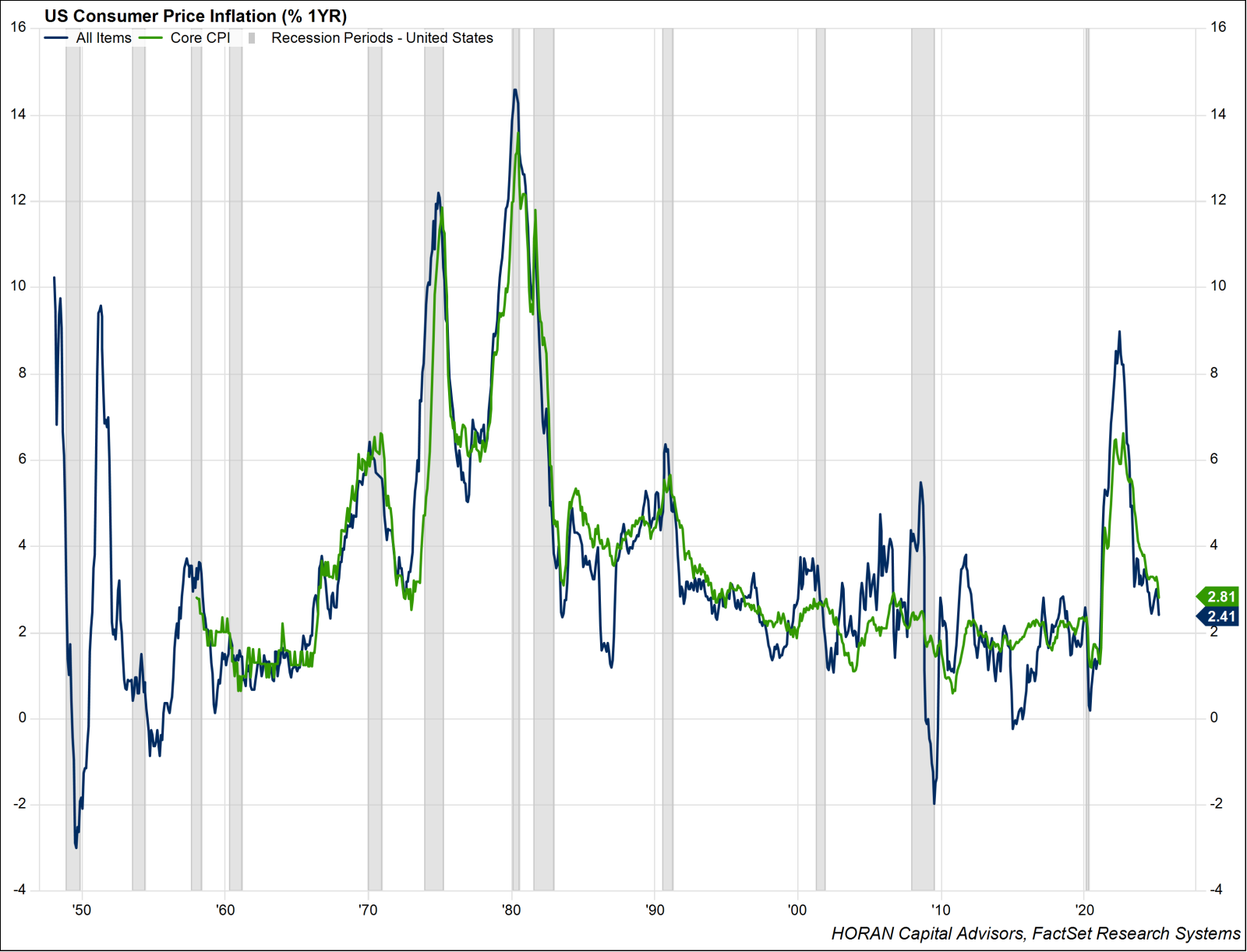

The Consumer Price Index for March declined to 2.4% Y/Y, this report was below the analyst estimates of 2.6%. This decline was primarily led by the recent fall in energy prices, with WTI Crude recently hitting a multiyear low. Additionally, Core CPI (CPI ex. Food & Energy) also decelerated to 2.8% Y/Y, led by a deceleration in Shelter prices.

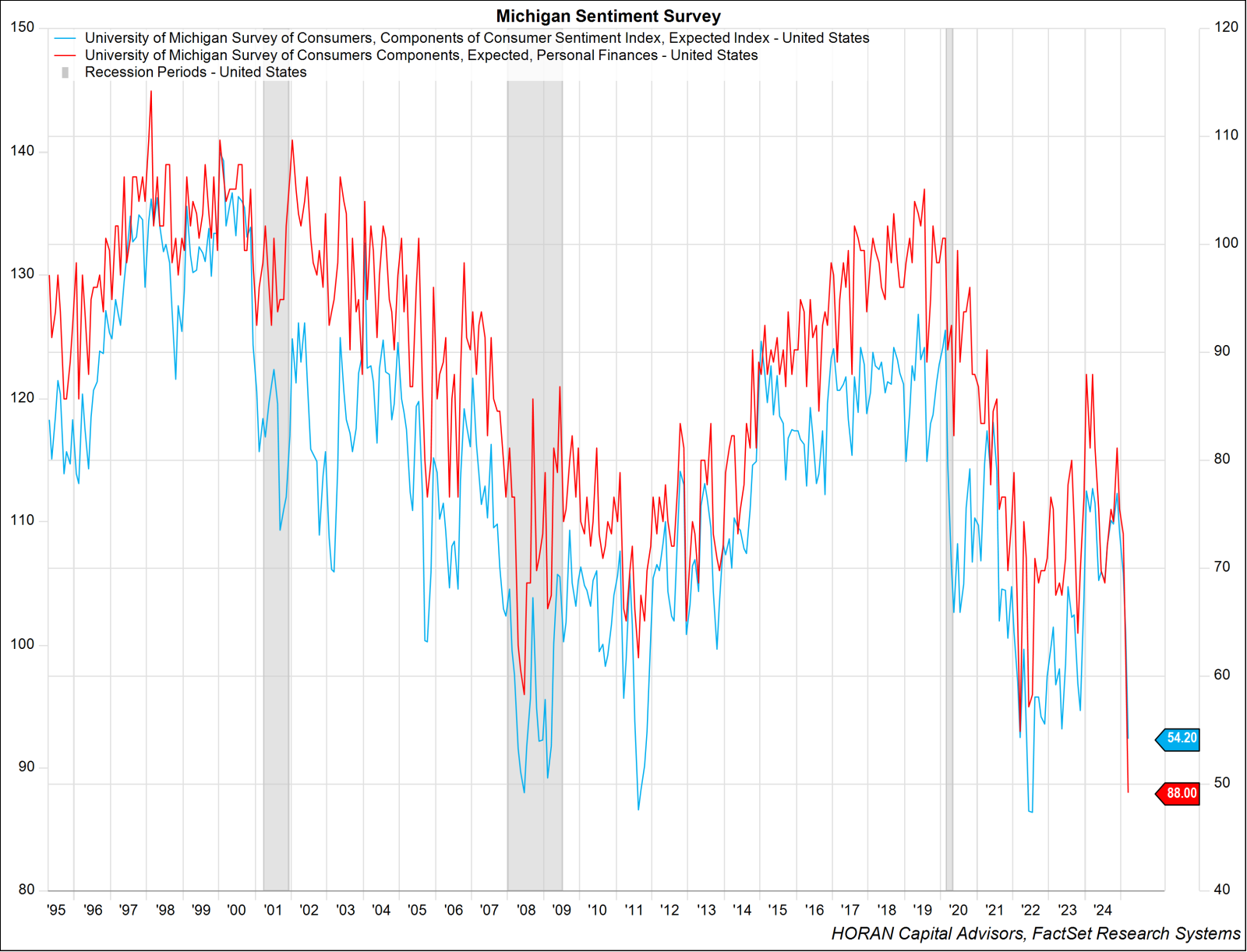

Preliminary results of the University of Michigan’s Survey of Consumers fell 11% in April, sentiment has now declined 30% since December. Consumer have begun to raise recession risk and weaker expectations for business conditions, personal finances, incomes, inflation, and labor markets. The expectation that unemployment is going to rise is now at its highest level since 2009.

FOMC Minutes – outlook weaker GDP as aggregate spending has been below estimates and financial conditions have deteriorated. Risks for reinflation have been mitigated given aggregate consumption.

The Week Ahead:

- Empire State Index (4/15)

- Retail Sales (4/16)

- NAHB Housing Market Index (4/16)

- Building Permits and Housing Starts (4/17)

- Easter – markets closed on Friday

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.