Author: Zac Martin, Investment Associate

Week Ending May 30th – Taco Tuesdays

GDP 2nd Preliminary reading for Q1 2025 was revised slightly higher (to -0.2%) than the previous report. Same idea here, imports outweighing consumption. Adjusting for imports, GDP consumption grew ~1.5%.

FOMC minutes for the May meeting highlighted the effect tariffs have had on the GDP calculation (inflated imports) but mentioned that Private Domestic Final Purchases reflected a stronger GDP report. Overall, the committee is expecting a slightly weaker economy but not a recessionary environment.

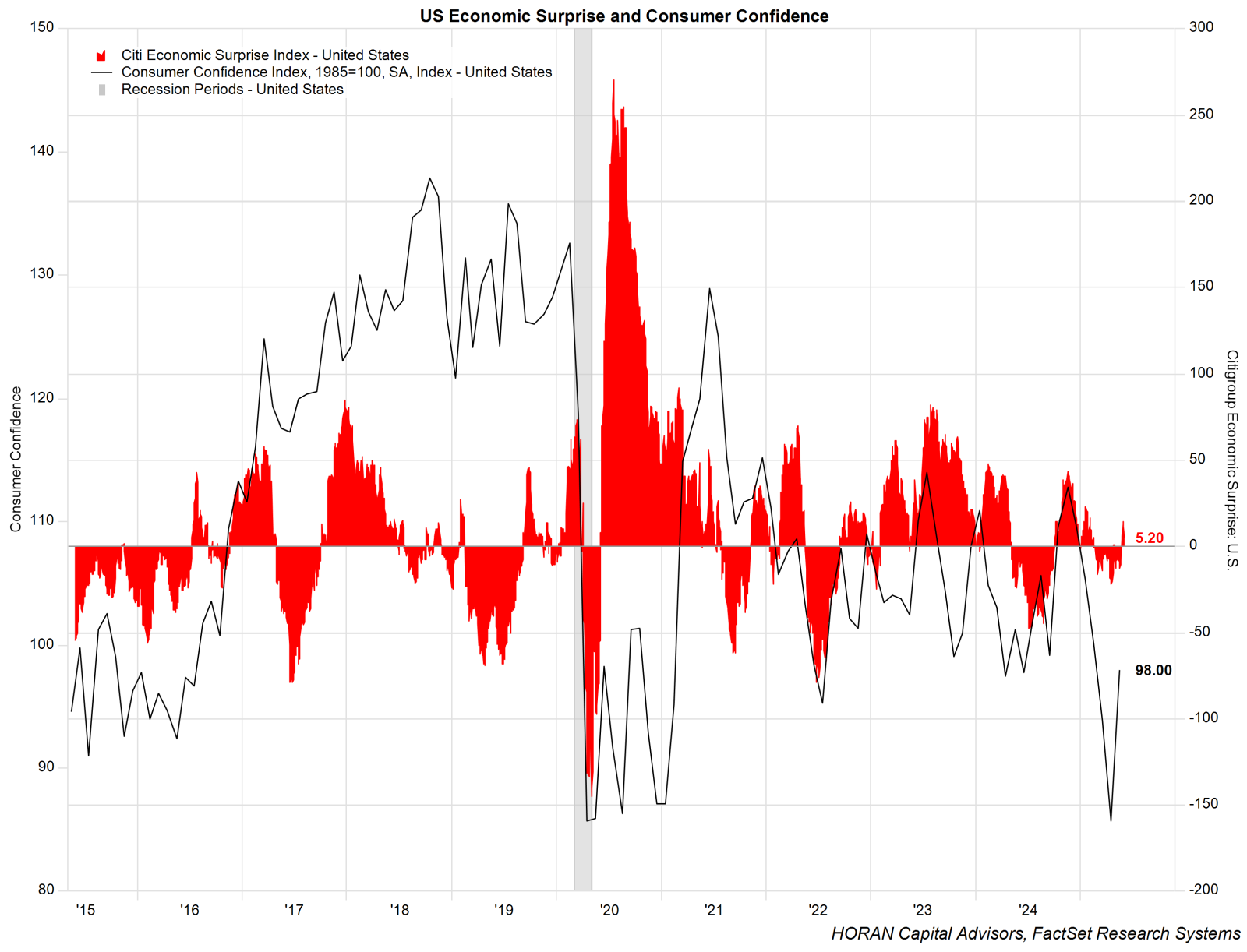

Consumer Confidence Index for May reported a 12.3-point increase, beating consensus estimates by 10 points. Write-in responses highlighted the still present concern around trade policy, but respondents remained hopeful for continued trade deals. The shares of consumers expecting a recession in the next twelve months declined and inflation expectations eased slightly.

The Week Ahead:

- ISM Manufacturing PMI & ISM Service PMI (6/4)

- JOLTS report (6/3)

- Nonfarm Payrolls & Unemployment Rate (6/6)

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.