Author: David I. Templeton, CFA, Principal and Chief Investment Officer

The Disruptive Nature of A.I. In The Job Market?

It seems one is unable to get through a day without news on how disruptive A.I. or Artificial Intelligence is to a company's products. This then leads one to contemplate the potential negative impact A.I. might have on employment at the company level and more broadly, the overall employment level in the economy. At the moment much of the reporting on A.I. assumes these A.I. programs will replace large swaths of positions in the job market. For example, Agentic A.I. represents an artificial intelligence system that can function autonomously and make decisions without human intervention. The Agentic A.I systems can create and monitor software code; hence, the reduced need for software coding engineers. Additionally, some A.I. programs can write code and create apps or software based on prompts by humans. All of this has led to a decline in software stocks as the moats for companies may not be as large as originally thought if these A.I. programs can create programs to compete with existing software products. Below is a chart of the iShares Expanded Tech-Software ETF (IGV) and clearly the decline accelerated in early February and on higher volume.

Contributing to this glass half empty view on employment was a report by an organization, Citrini Research. The author published a research report from the perspective of the future with the artificial future date of June 2028. The report titled, The Consequences of Abundant Intelligence, begins by noting the unemployment level in the U.S. is 10.2% and rising. And an excerpt from the report:

It should have been clear all along that a single GPU cluster in North Dakota generating the output previously attributed to 10,000 white-collar workers in midtown Manhattan is more economic pandemic than economic panacea. The velocity of money flatlined. The human-centric consumer economy, 70% of GDP at the time, withered. We probably could have figured this out sooner if we just asked how much money machines spend on discretionary goods. (Hint: it’s zero.)

AI capabilities improved, companies needed fewer workers, white collar layoffs increased, displaced workers spent less, margin pressure pushed firms to invest more in AI, AI capabilities improved…

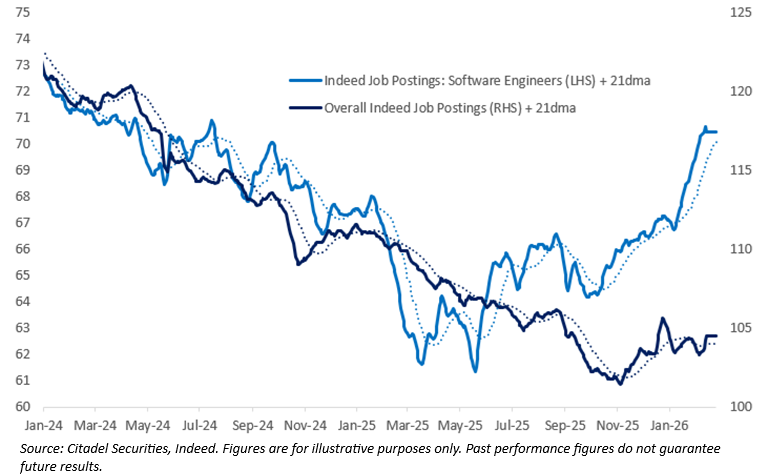

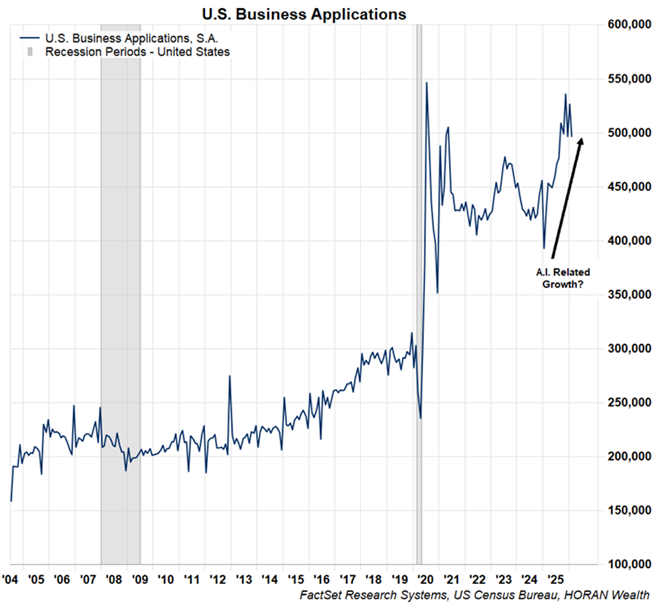

The full Citrini Research report portrays a doomsday type prediction for the economy resulting from the success of A.I. programs. Ken Griffin's Citadel Securities followed up with a report countering the Citrini report titled, The 2026 Global Intelligence Crisis. This report highlights the increase in job postings for software engineers as well as the growth in new business formation, both charts below. A.I. does not seem to be detracting from the job market and business growth. These two variables are hard data points too.

A.I.'s Positive Implication for Businesses

And lastly, two podcasts worth listening to address the software issue and the disruptive nature of A.I. The first podcast by Torsten Slok, Partner and Chief Economist at Apollo and titled The U.S. Economy: Resilience under Pressure, notes many positives expected to result from companies incorporating A.I. programs into their businesses. Torsten also highlights the growth in the number of new businesses and the resulting growth in more jobs. He mentions the fact A.I. can more quickly uncover problems impacting companies; thus, greater employment is needed to have individuals in place to address the additional problems. He also notes, "Technology innovation over the last 50 years has always resulted in human ingenuity, coming up with more ideas, more ways to do things, and ultimately being good for the economy and therefore good for employment."

Technology Risk in One's Investment Portfolio

For investors he points out that much of the growth in A.I. is occurring in the U.S. For example, the U.S. has 6,000 data centers and this is more than all other countries combined. There is risk though. Historically, one invested in a 60/40 portfolio, i.e., 60% equity and 40% fixed income for diversification purposes. If stocks went down, generally bonds would go up and vice versa. Today, the U.S. equity portfolio is highly concentrated in A.I. or technology related stocks. Nearly 40% of the S&P 500 Index is comprised of technology or technology adjacent companies. In the fixed income or bond portfolio, a large portion of the bond portfolio is technology related companies verse twenty years ago. In other words, investors are receiving less sector diversification in a broad 60/40 portfolio. Torsten discusses how international investments do provide diversification away from technology as most technology companies are headquarter in the U.S.

Finally, given the recent hit to software stocks, Goldman Sachs' Gabriela Borges discusses key factors to evaluate with software stocks in her recent podcast, Can Software Survive AI? Software companies, where A.I. is creating a headwind for their stocks, do have tools and business structures that have been developed over time that can't be replicated by an A.I. program alone. As Gabriela notes AI likely augments rather than fully replaces software. Current software companies that have proprietary data and access to existing endpoints/users may survive better than expected, while 'AI-native' startups face higher barriers than anticipated. A key differentiation for existing software companies is whether they have pricing power or not. The podcast, just 15 minutes in length, is a worthwhile one to listen too.

In conclusion and in my view, A.I. will be additive to employment and economic growth. This has been the case in prior economic periods like the industrial revolutions and the technological revolution. Certainly, existing companies will need to be mindful of the changes resulting from A.I. and look to incorporate AI in their businesses. Otherwise, new companies will challenge and disrupt the markets where they do business.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.