David I. Templeton, CFA, Principal and Chief Investment Officer

Investors analyze investment opportunities by evaluating the forward prospects of a stock or an index. This strategy requires analyzing forward-looking data over a one-year horizon, and frequently stretching out across a three- and five-year timeframes.

The Concentration Risk of Top-Heavy Leadership

The recent strong performance of the S&P 500 Index—which is up 8.14% year-to-date, 24.3% over the past year, 20.8% annualized over three years, and 12.4% annualized over five years, has been driven largely by the "Magnificent 7" (MAGS) mega-cap stocks.

This narrow leadership has created historic concentration risks within the benchmark:

- The Top 10 Holdings: Now command a significant 41% of the total index weighting.

- The Magnificent 7: Accounts for 34.5% of the index weighting alone.

- Investor Inflows: For every dollar that flows into an S&P 500 index fund, 41 cents is automatically allocated to the top ten stocks, with 34 cents concentrated into just the seven mega-cap stocks.

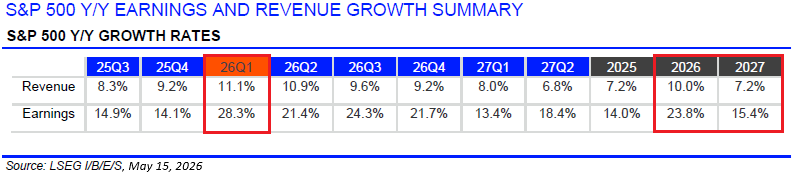

The 2026 Earnings Tailwinds

Supportive of the overall advance in the S&P 500 Index is the growth of earnings in 2026. At the beginning of the year expected earnings growth for first quarter equaled 14.4% with growth for all of 2026 expected to equal 15.6%. With first quarter 2026 earnings reports nearly complete, year over year earnings in the quarter equals a growth rate of 28.3%. For all of 2026 the expected growth rate for Index earnings is now 23.8%, more than 50% higher than expectations at the beginning of the year.

The Foggy 2027 Outlook: Deceleration and Valuations

One factor that can serve as a headwind for stocks is an environment where earnings growth is slowing. As seen in the above earnings table, expectations are 2027's earnings growth for the S&P 500 Index will be lower than the growth rate expected in 2026. A primary headwind for equities can be a transition into a decelerating earnings growth environment.

- Slowing Sectors: Industrials, Communication Services, Materials, and Information Technology are expected to experience the sharpest growth deceleration.

- Contraction Sectors: The Energy sector is currently projected to experience an absolute earnings contraction.

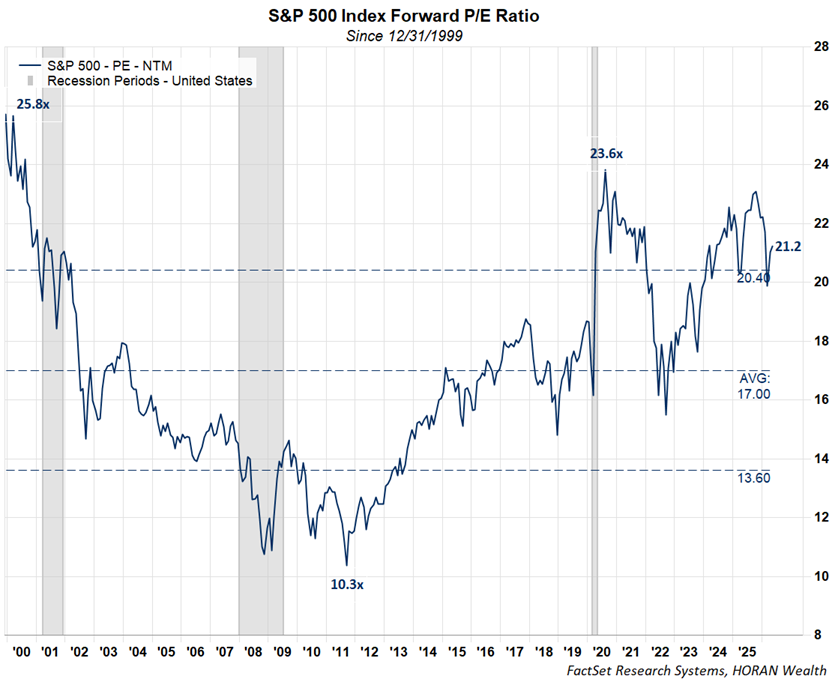

Further, the slowing growth rate in earnings can have a negative impact on stocks and more so for stocks trading at high valuations. For the S&P 500 Index, the forward price to earnings ratio is currently about 21 times and is slightly above one standard deviation from its mean. This is not at an extreme, but valuations are broadly elevated.

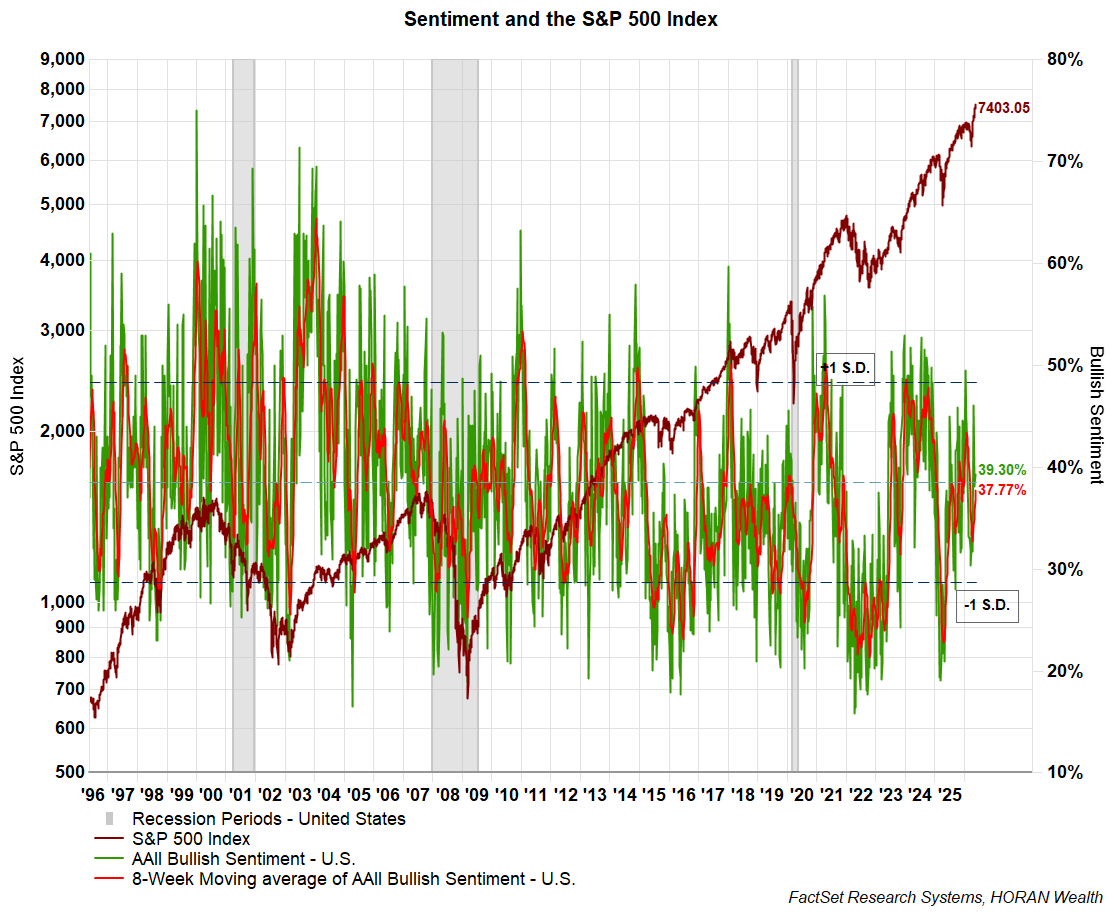

Importantly, earnings are expected to see mid-teens growth in 2027. This is a positive, especially in light of the fact it does not appear individual investors are overly bullish based on the AAII Sentiment Survey with the bullish ready at 39.3%, near the long run average. Sentiment surveys are contrarian ones and if investors express overly bullish sentiment, this would be a negative market observation.

Inflation and Interest Rates

The trajectory of intermediate and long-term interest rates remains an important variable for equity valuations. The underlying catalyst behind rising bond yields will dictate market stability:

- Growth-Driven Rate Hikes: If interest rates rise because of accelerating economic expansion, the negative impact on corporate equities probably remains minimal.

- Inflation-Driven Rate Hikes: If higher yields are triggered by stubborn inflation expectations, equities can face a strong headwind.

Higher inflation-driven yields undermine stocks in two ways. First, the higher yields make bonds an increasingly more attractive, lower-risk alternative to equities. Second, higher anticipated inflation will result in analysts raising the discount rate applied to corporate earnings models. This adjustment lowers the present value of future cash flows, putting downward pressure on equity valuations.

Looking ahead then, future earnings reports will be important to evaluate, especially in light of the significant increase in capex from technology companies expanding in the A.I. space. Additionally, with a new Fed chair coming on board at the Federal Reserve, this change has historically resulted in higher equity volatility regardless of the new Fed chairs policy positions.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.