Author: David I. Templeton, CFA, Principal and Portfolio Manager

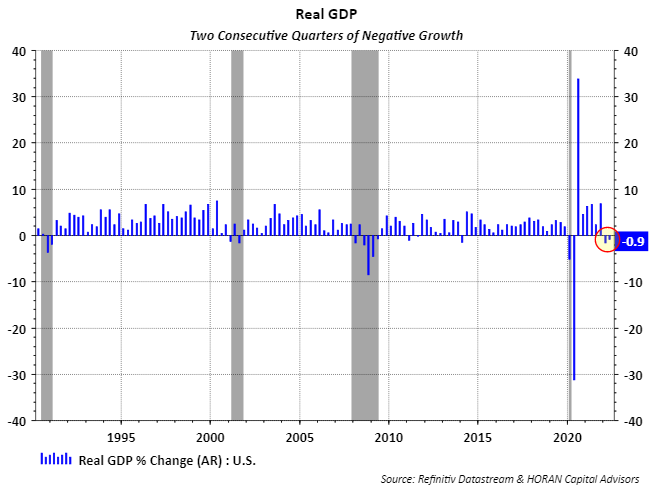

Undoubtedly the current investing environment for investors is as tough a one as there has been for some time. Compounding interpretation of the data now is the issue of the pandemic and the consequences of an ill advised global economic shutdown. Governments and businesses around the world are finding out how difficult it is to restart a global economy that, in more recent times, has relied on just in time inventory management. Bottlenecks, backlogs and shortages seem difficult to eliminate. The fiscal and monetary actions employed to counteract some of the effects of the shutdown have led to inflation rates last seen some forty years ago and central banks around the world are raising interest rates in response. For the U.S. Federal Reserve, higher interest rates or monetary tightening historically has led to economic recessions. In fact, at the end of July, the advanced reading for second quarter real GDP has the U.S. economy contracting at an annual rate of minus .9% and follows Q1 2022 real GDP of -1.6%. Two consecutive quarters of negative real GDP is the technical definition of a recession.

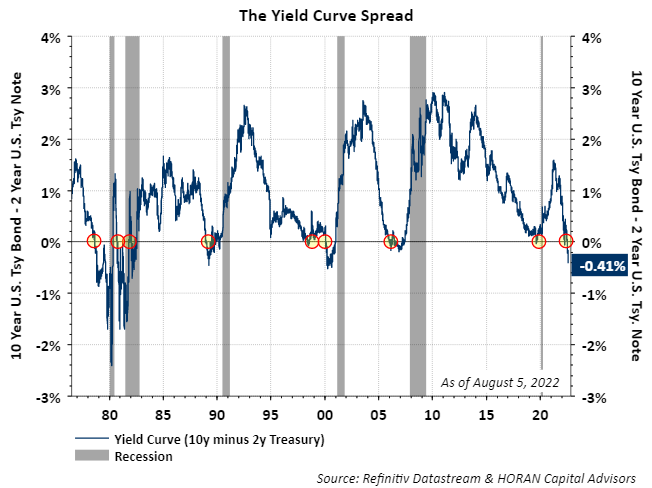

Further, the Federal Reserve's tightening of monetary policy through higher short term interest rates, has led to the 10 year Treasury Yield less the 2 year Treasury Yield turning negative, i.e., an inverted yield curve as seen in the below chart. The grey shaded areas on the chart are recessions and recessions have mostly followed inverted yield curves, on average, about one and a half years following the inversion.

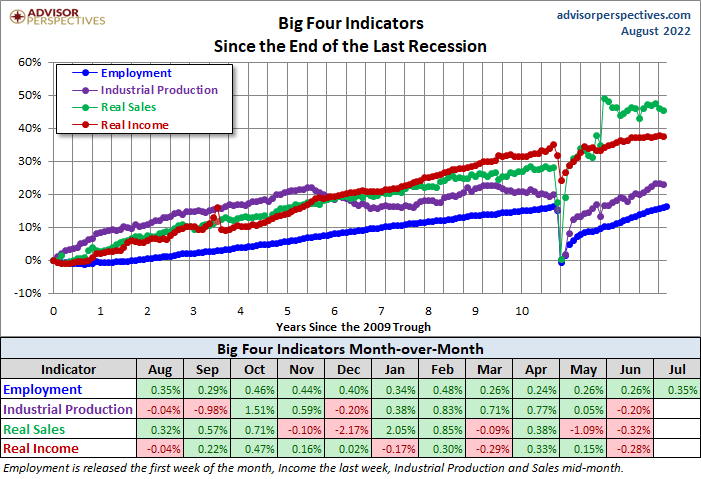

Some economist contend two quarters of negative GDP alone are not a sufficient indication of a recession. Certainly, other variables can come into play. At the Advisor Perspectives (AV) website, there are other metrics that are evaluated and AV refers to these metrics as the 'Big Four' indicators. As the below table shows, three of the four indicators are experiencing month over month (MoM) declines with the employment indicator continuing to improve on a MoM basis.

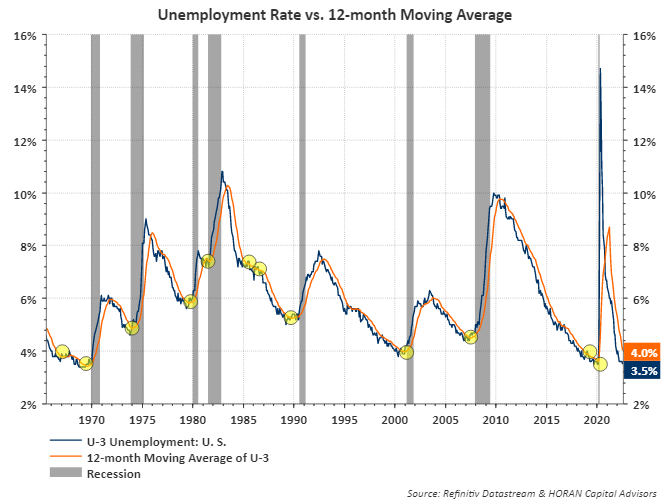

In fact last week's report on July nonfarm payrolls showed an upside surprise of 278 thousand for a total payroll increase of 528 thousand in the Establishment Survey. In the Household Survey in the same report, payrolls increased only 179 thousand and payrolls from the household survey are down about 136 thousand since May's report and it is the household survey figures that are used to calculate the unemployment rate. Employment is a lagging indicator and tends to be one of the later variables that deteriorates as a recession nears. Below is a chart of the unemployment rate measured against its 12-month moving average. Recessions tend to be forthcoming if the rate crosses above the 12-month moving average and is one of the charts we evaluate for determining the onset of a recession.

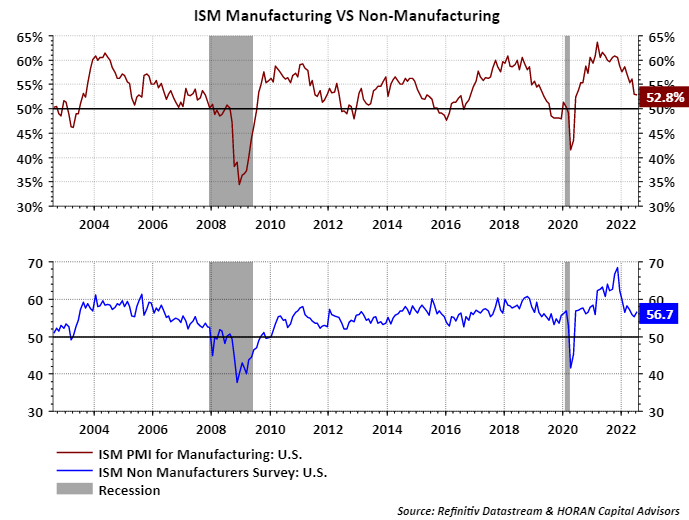

Within the last week or so both the ISM manufacturing and nonmanufacturing reports were released. A weakening trend continues to unfold in the manufacturing data, but the diffusion index remains above 50% which signals an expansionary manufacturing sector. The nonmanufacturing or services index ticked higher to 56.7% and is an expansionary indication too. Services account for about 70% of economic activity or GDP so an increasing nonmanufacturing index is not signaling a recession. Additionally, the prices paid component of both indexes is showing improvement, potentially providing some relief on the inflation front as well.

As it relates to the equity market, I have written a couple of articles, here and here, about June possibly being the low in this bear market pullback. Last week the S&P 500 Index ended higher by 37 basis points and was the third consecutive week for positive returns for the index. Since the June 16 low the S&P 500 Index is up 13.1% leaving it down 13% this year. As the below chart shows, the index is moving higher within a channel, creating higher lows and higher highs, that has the Index overcoming resistance at the 21 and 50 day moving averages. The next hurdle seems to by resistance at the 4177 level.

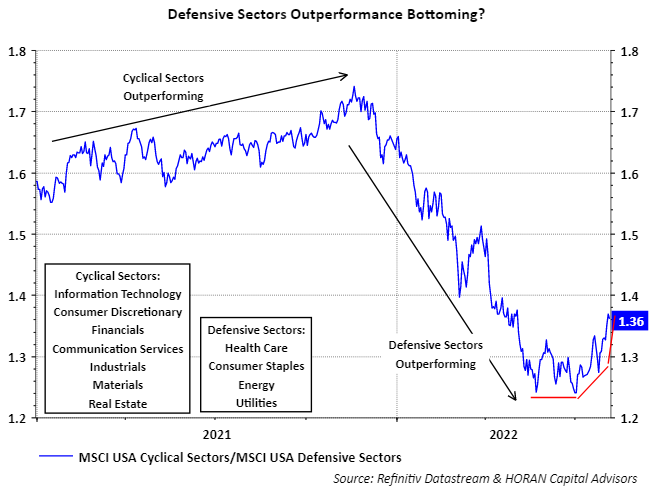

And lastly, since the beginning of July the cyclical sectors of the market are outperforming the defensive health care, staples, energy and utility sectors as seen below.

Importantly, the equity market has experienced a pullback that may have bottomed in June. The S&P 500 Index itself is a component of the Conference Board's Leading Economic Index, as such, any anticipated economic weakness may get reflected in assets prices earlier than a bottoming of the economy. Also, inflation pressure remains an issue and investors receive July's CPI report later this week. It is often said that the economy and the stock market are not the same. Certainly, some market sectors and industries bottom before the economy and/or can do well in a recession. As noted at the outset of this article this is a difficult environment for investors. Maintaining patience and sticking to a discipline is important to navigate the market's volatility regardless of whether the economy is in a recession or not.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.