Author: David I. Templeton, CFA, Principal and Portfolio Manager

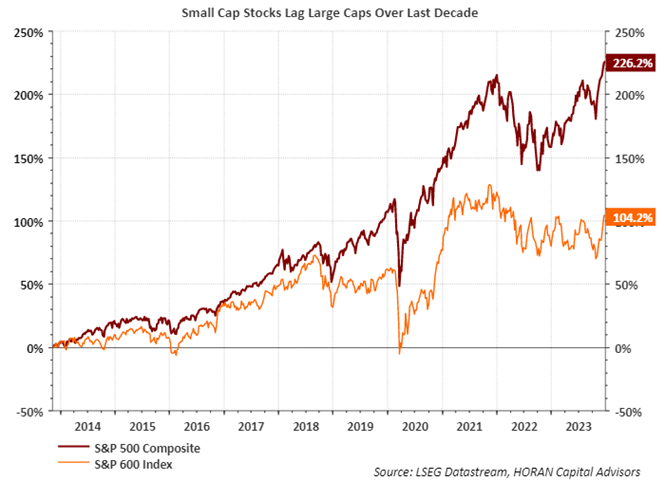

With much of the attention placed on a few mega cap stocks, partly due to their focus on artificial intelligence (AI,) among other favorable operational businesses, asset class categories outside of the large cap segment have lagged in performance. Specifically, small company stocks have not enjoyed the same level of return that larger company stocks have enjoyed. As the below chart shows, the S&P Small Cap 600 Index return since 2013 is less than half the return of the large cap S&P 500 Index.

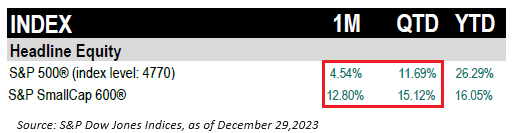

However, since near the end of the third quarter in 2023, small cap stock returns have outpaced the large cap segment, having accelerated its outperformance in December.

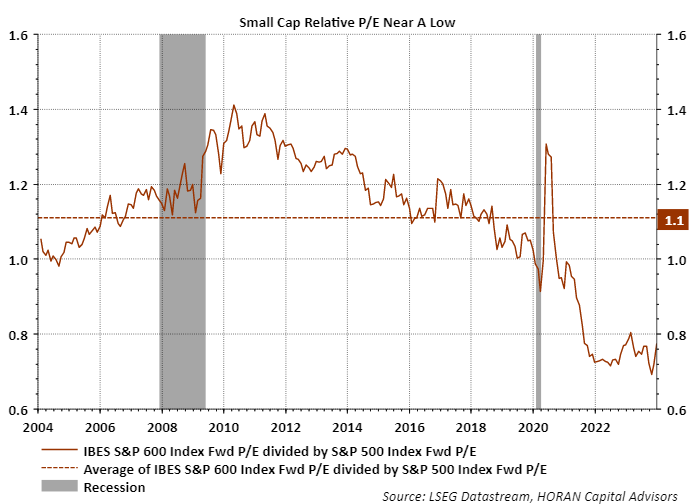

Simply because a specific asset class has underperformed others over an extended period of time does not necessarily mean the underperforming one will begin to outperform going forward. The same can be said for valuations. However, if valuations are significantly lower than valuations in alternative asset classes, the margin of safety is greater. Or said another way, the risk reward of the lower valued asset class is better. To that end, the relative valuation of the S&P Small Cap 600 Index compared to the S&P 500 Index is near a record low.

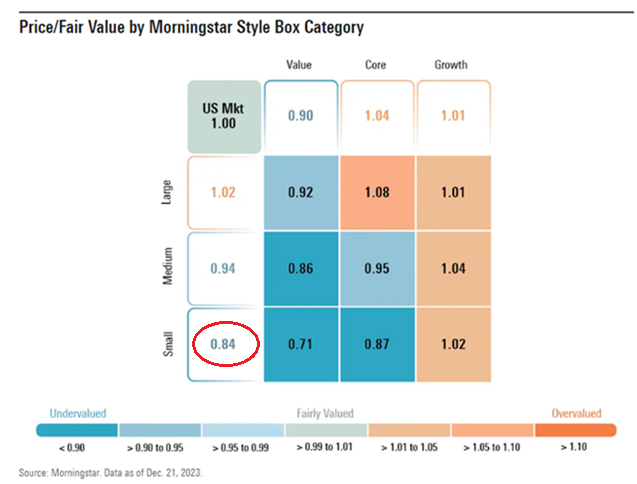

Lastly, in a recent Morningstar article, 2024 Market Outlook: What a 'Return to Normal' Means for Stocks, the outlook highlights the attractiveness of small company stocks. In the article, a graphic details the Price/Fair Value for various market cap levels. The most undervalued style category is small company stocks as seen below.

As noted in the article:

"By capitalization, small-cap stocks remain the most attractive at a 16% discount, followed by mid-caps at a 6% discount, while large caps are a little above fair value. On a price/fair value basis, small-cap stocks remain near some of the greatest discounts to large-cap and mid-cap stocks that we have seen since 2010. Small-cap stocks sold off harder and faster during the early stages of the pandemic as investors feared smaller companies would not have the wherewithal to survive. This past fall, small-cap stocks were under additional pressure as investors were concerned that small-cap stocks would be more adversely affected by rising interest rates as they typically have shorter duration debt and may need to refinance at high interest rates. In addition, bank funding has become more restrictive as banks are less willing to extend loans to higher risk credits. In our view, this sets the stage for small-cap stocks to outperform."

As sometimes said, 'time will tell' if small caps do generate outperformance versus the larger capitalization asset classes. If the fourth quarter of 2023 is any guide though, 2024 just might be a year that rewards investors allocating some funds to the small cap asset class.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.