Author: David I. Templeton, CFA, Principal and Portfolio Manager

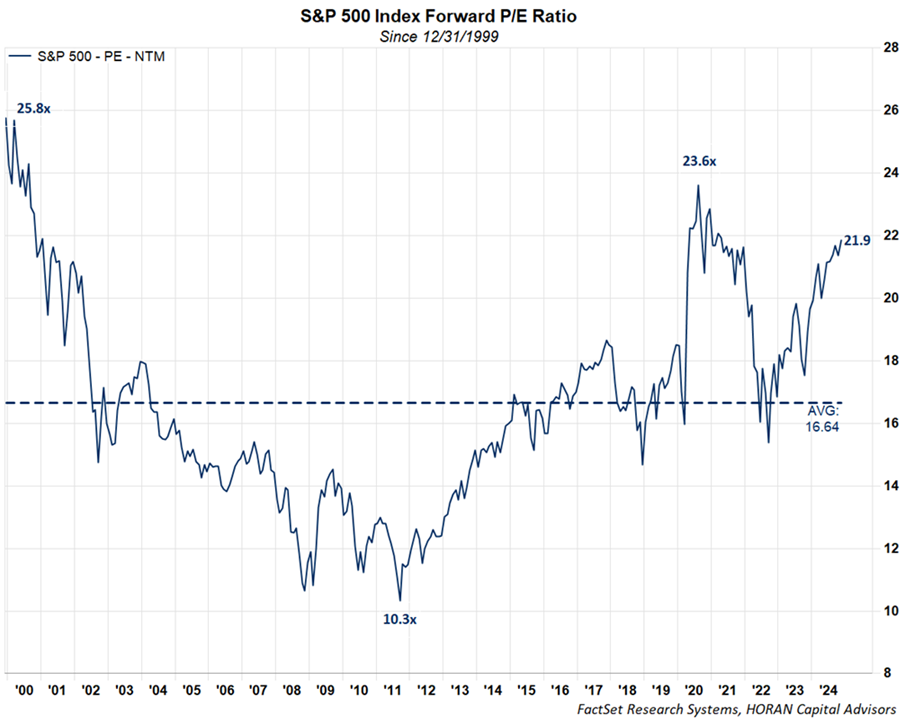

The S&P 500 Index has enjoyed strong returns in 2023, up over 26%, and year to date in 2024, up over 23%. Earnings growth has been strong up low to mid-teens percentage as well, but the index return has outpaced the growth in earnings resulting in the market's valuation becoming stretched. As the below chart shows, going back to 1999, the current price earnings ratio, or P/E, of 21.9 times is near the level reached in 2000.

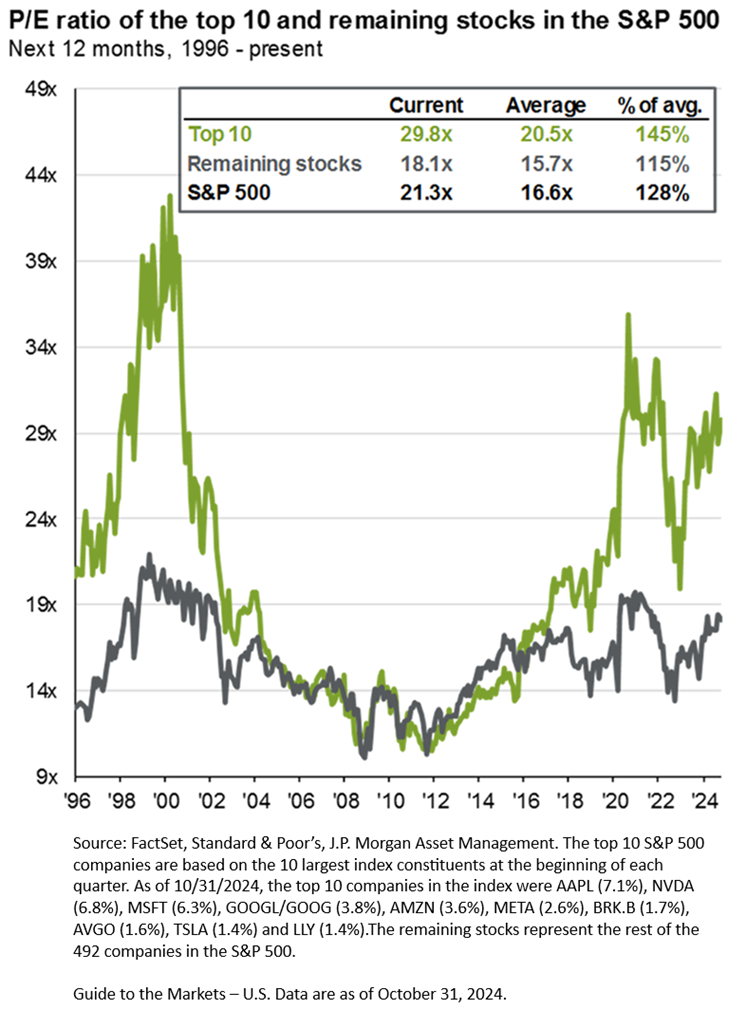

Worth noting is the equity market generally does not correct simply based on valuation. With the valuation of the mega cap stocks extended, and many of the largest stocks technology ones, the market excluding the Top 10 are not as elevated.

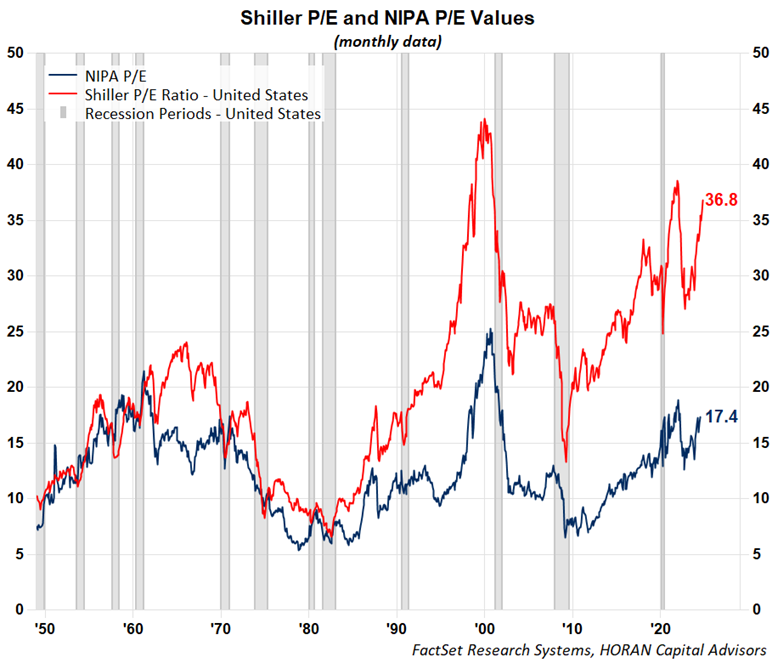

One valuation metric known as the Shiller Cyclically Adjusted P/E ratio or CAPE, was developed by Robert Shiller. In arriving at the earnings component in Shiller's Price Earnings ratio, Shiller valuation measure uses the average of the last 10 years of earnings adjusted for inflation. The advantage of this is it smooths swings in earnings from year to year. On the other hand, earnings might be down in one particular year for a unique reason and the CAPE ratio might remain elevated when in actuality the one-year event might represent a good buying opportunity for equities.

Another valuation measure is the NIPA P/E ratio. This uses corporate profits from the GDP report for the earnings. In essence corporate profits from the GDP report captures all profits for businesses that are used in the calculation of GDP each quarter. The latest corporate profit figure comes from the second quarter report as this figure is reported by the Bureau of Economic Analysis in the second report for GDP. The third quarter update for profits will be available near the end of November. As the below chart shows, the Shiller CAPE ratio is nearing the high reached just after the pandemic. and the NIPA P/E is rising in a similar fashion. Both have not reached the highs in the technology bubble period in 2000.

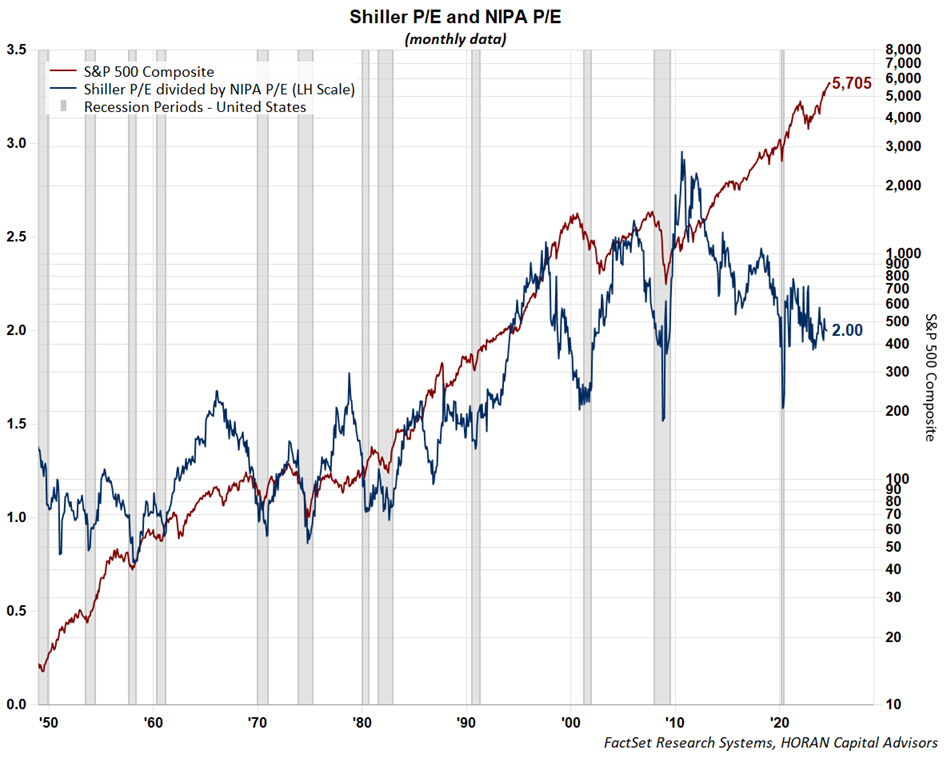

Finally, evaluating the ratio of the Shiller CAPE ratio to the NIPA P/E ratio, one sees the NIPA P/E is rising at a faster pace than the Shiller P/E given the declining ratio as seen with the blue line in the below chart. Interestingly, when this ratio nears its historical cycle low, i.e., a high NIPA P/E relative to the Shiller P/E, the chart indicates this is a good time to add to equities. At lower NIPA P/E levels and a higher relative Shiller P/E, this tends to occur near intermediate market tops. Is a high ratio of the two P/E's indicative of a market that is anticipating peak earnings? Conversely, is the lower ratio one where the market anticipates earnings will improve; thus, a good buying opportunity for equities?

In regards to earnings, forward earnings for the S&P 500 Index are shown below and there is some truth to the fact that stocks prices follow earnings over time. Additionally, with the new administration in Washington, D.C. at the start of next year, a potential tax policy change may occur. One area of change is a reduction in the corporate tax rate which would mean higher after-tax earnings for firms. An increase in tariffs could offset some of the tax reduction benefit, but net net, higher earnings are likely if corporate tax rates are reduced. Higher earnings equate to lower stock valuations and some repricing of stocks higher recently may be in anticipation of this occurring and might continue into year end.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.