Author: David I. Templeton, CFA, Principal and Portfolio Manager

The theme of my Tuesday blog article was the fact investors have a high allocation to stocks relative to history and this could be a symptom that exacerbates a market pullback. Also, noted in the earlier post, the Conference Board's consumer survey noted a record percentage of respondents stated stocks would be higher over the course of the next 12-months. A conclusion in the earlier post, with sentiment measures being contrarian ones, and with high equity allocations, a pullback in stocks would not be a surprise. As is the case with a number of economic data points though, data reported for investors' exposure to stocks is mixed too.

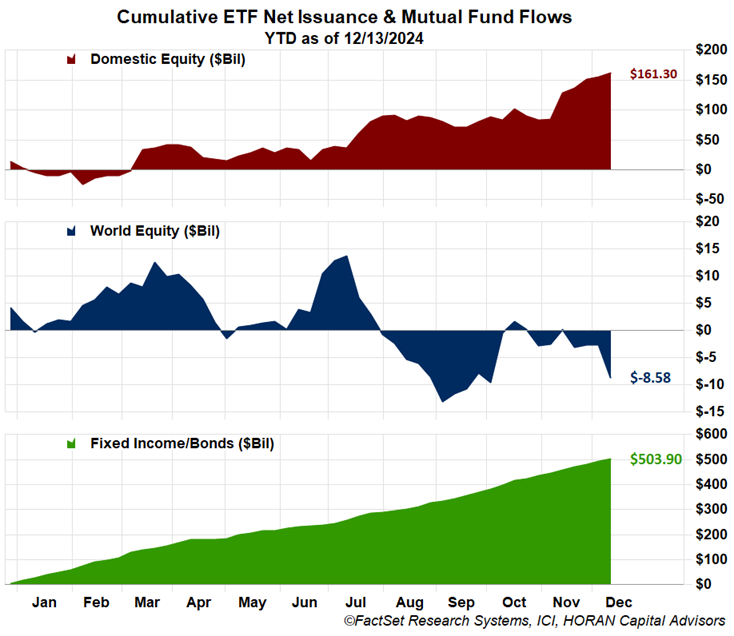

In reviewing the fund and ETF flow data in the below chart with data provided by the Investment Company Institute (ICI), ETF issuance and mutual fund flows this year have seen U.S. equities take in $161.3 billion yet flows into fixed income investments over the same period total $503.9 billion. Just these two measures by themselves do not seem to indicate investors are favoring stocks over bonds.

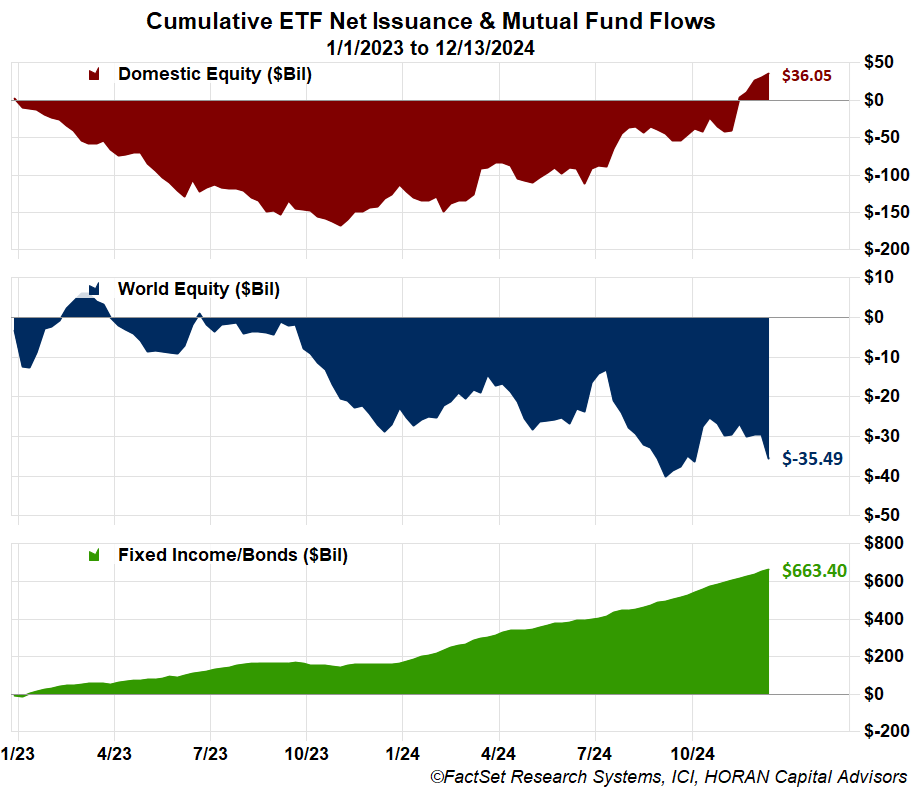

Looking at a little longer time frame of about two years, the below chart shows only $36.1 billion has flowed into U.S. equities compared to $663.4 billion flowing into bond investments. The upward trend on the domestic equity flows since October of 2023 signifies positive flows into stocks since that time.

The one asset class that has grown substantially since 2023 is money market assets. As seen in the below chart, at the beginning of 2023 assets in money market funds totaled a little more than $4.5 trillion and today total nearly $6.8 trillion. These cash funds can certainly serve as support for stocks when the equity market experiences a pullback as some of the cash may find its way into stocks.

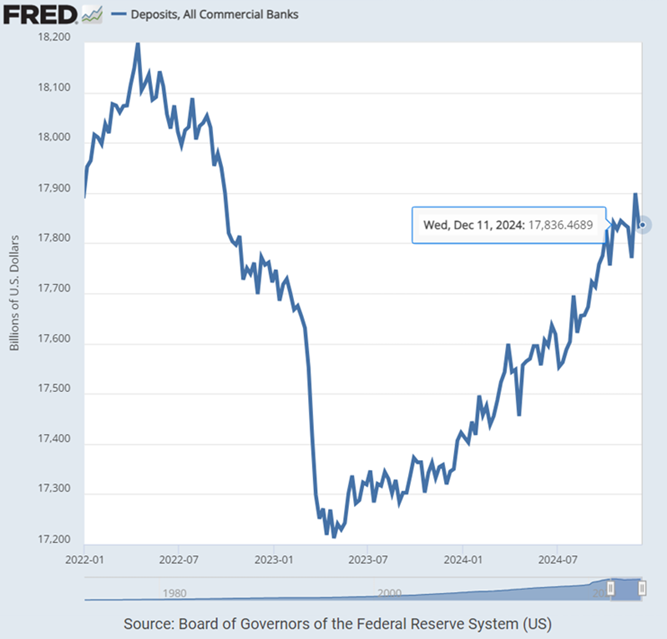

And finally, it gets pointed out from time to time that the money market assets simply were flows out of the banks since they were paying such low rates of interest. This is partially true as the banks were slow to raise interest rates on deposits at a time the Fed was rapidly increasing the Fed Funds rate in 2022. However, as seen below, the out flows from banks reversed in the summer of 2023 and bank deposits have been increasing since that time while at the same time, money market inflows continue to rise. So, unlike the bearish data highlighted in the Tuesday post, as long as the economy continues to chart an expansionary path, stocks can continue to move higher, but not in a straight line. At the end of the day then, one might need to decide if the glass is half full or half empty as it relates to the equity market.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.