Author: David I. Templeton, CFA, Principal and Portfolio Manager

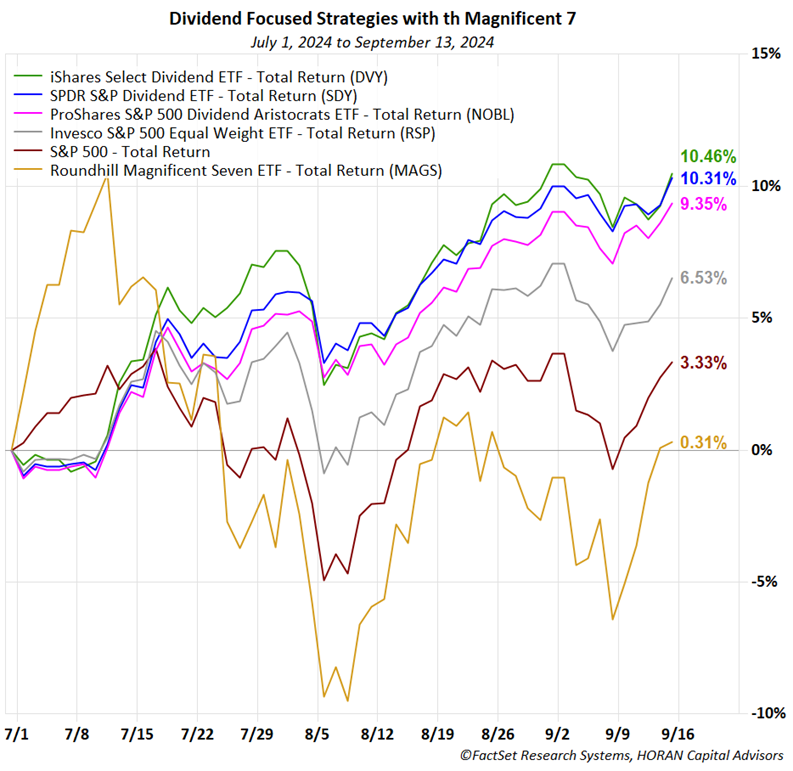

A large portion of the market's large cap return this year has been driven by the performance of the Magnificent Seven stocks. Not uncommon in September and October is elevated market volatility with third quarter to date returns being volatile from week to week. As the third quarter is nearing an end though, a broadening of stock participation is occurring in the market. As the below chart shows, some of the best performing areas in the market on a quarter to date basis are the dividend payers. Out of the six categories shown in the below chart, the four best performers are the dividend paying strategies and the equal weighted S&P 500 Index (RSP). The worst performing category is the Magnificent Seven (MAGS) stocks.

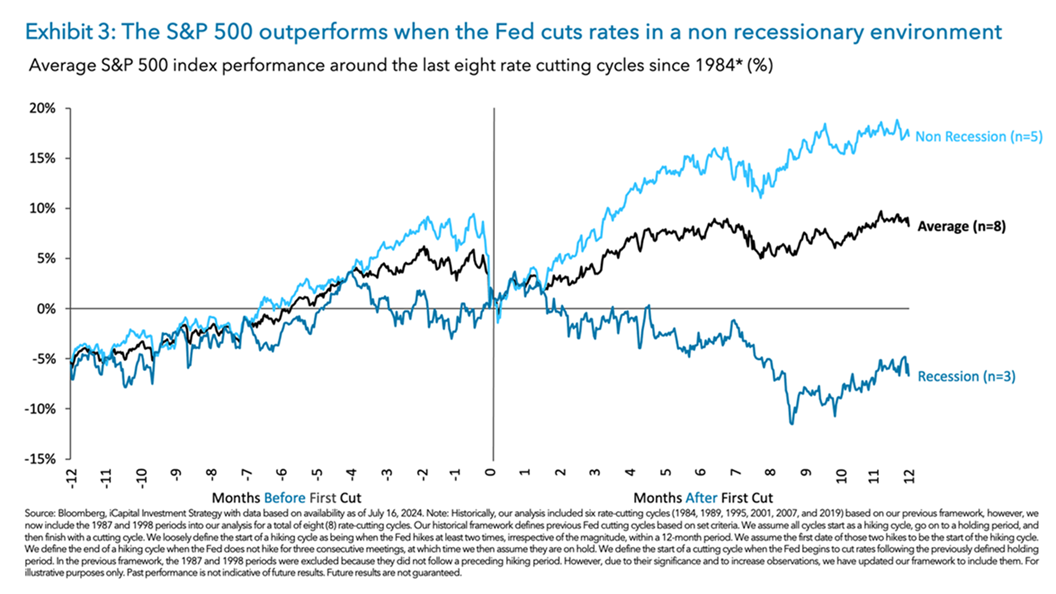

With a Fed rate cut expected this week, the debate is whether the Fed cuts 25 basis points or 50 basis points. The equity market tends to do well following a cut so long as the economy is not in a recession. Various versions of the below chart have been highlighted recently by strategist, but the chart does show historically the S&P 500 Index does well after rate cuts so long as the economy is not in a recession. At this point in time the economy's growth appears to be simply slowing to a pre-pandemic growth rate.

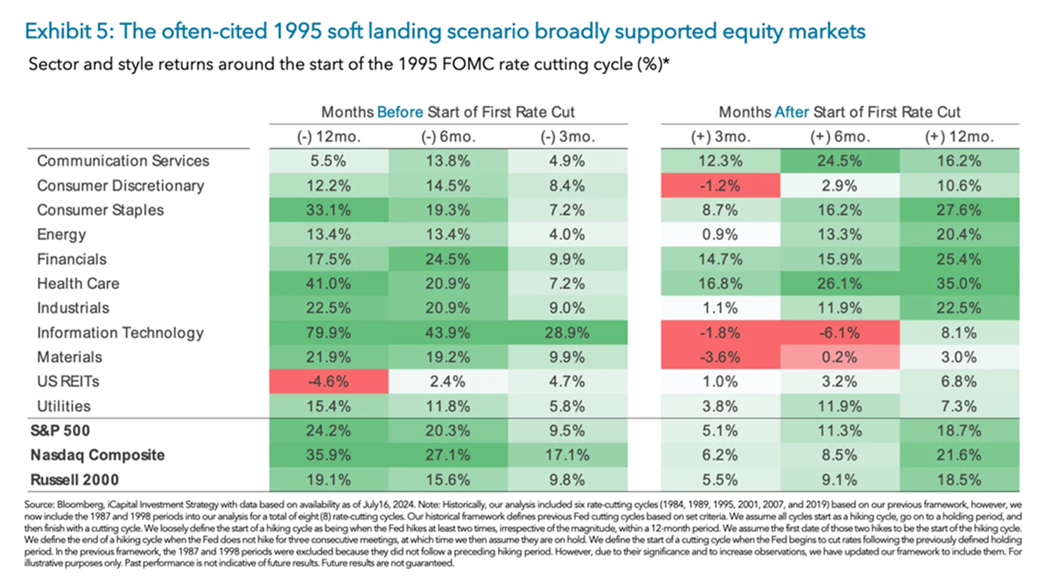

Also important are what areas or sectors of the market perform better after the rate cut. The below chart from a recent iCapital report shows Consumer Discretionary, Information Technology and the Materials sectors tend to be laggards following rate cuts. The stronger performing sectors historically are Health Care, Consumer Staples, Financials and Energy. This sector rotation is supportive of potentially more rotation away from the Magnificent Seven stocks. Granted, the artificial intelligence (A.I.) theme driving the strength of some stocks benefiting from this business does not seem to be going away, but prices for some A.I. related stocks may have gotten ahead of themselves near term.

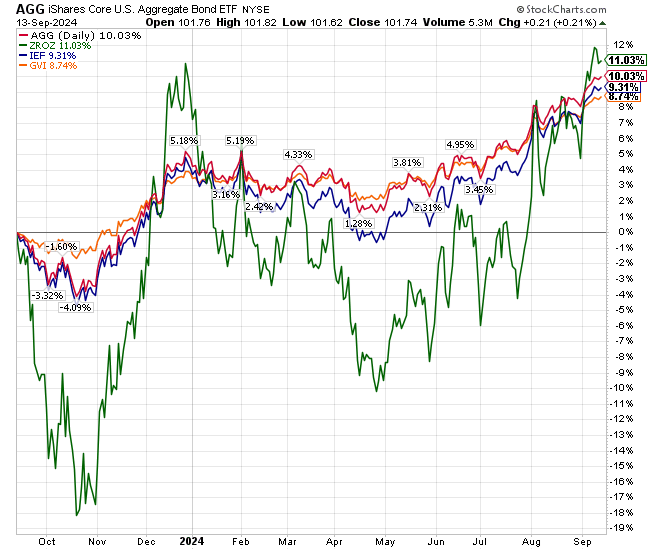

A segment of the market benefiting directly from interest rate cuts is the bond market since bond prices rise as rates decline. The 2-year U.S. Treasury yield has fallen from over 5% at the beginning of May to under 3.6% now. A large part of the bond return benefit may have already occurred as investors anticipated the cuts likely occurring this week. This decline has served as a tailwind for bond returns as seen in the below chart.

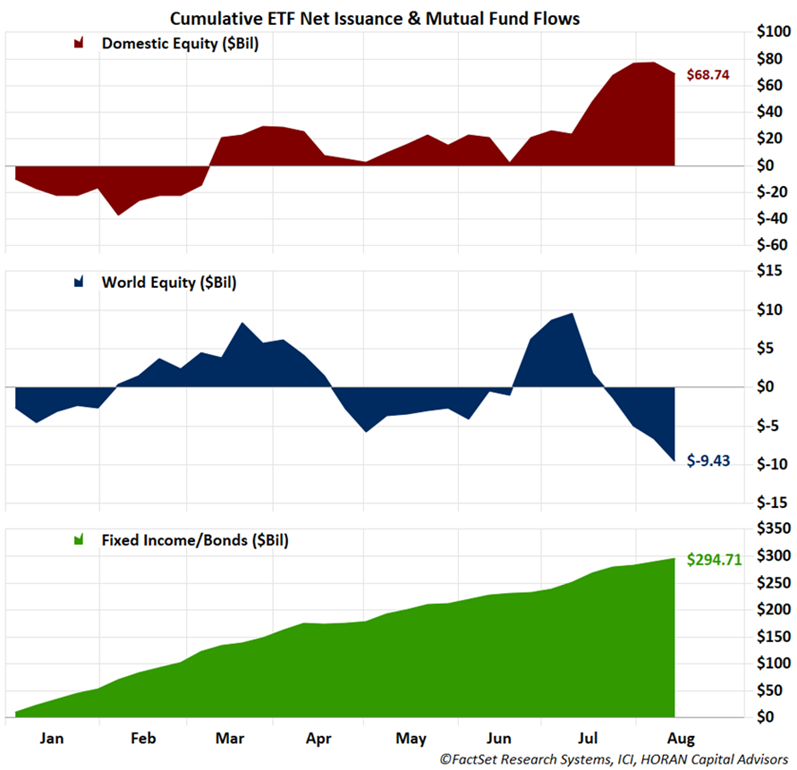

This anticipation can be seen in the flow of investment dollars into mutual funds and ETF's. On a year-to-date basis fund flows into bond funds and ETF's equals $294.7 billion while domestic equity flows equal $68.7 billion.

This week might see elevated market volatility due to the Fed rate decision coming on Wednesday as well as it being a triple witching week for options. Then throwing in all the potential election rhetoric, it is incumbent that investors focus attention on their longer-term investment goals and not the day-to-day noise.

HORAN Wealth, LLC is an SEC registered investment advisor. The information herein has been obtained from sources believed to be reliable, but we cannot assure its accuracy or completeness. Neither the information nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Any reference to past performance is not to be implied or construed as a guarantee of future results. Market conditions can vary widely over time and there is always the potential of losing money when investing in securities. HORAN Wealth and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. For further information about HORAN Wealth, LLC, please see our Client Relationship Summary at adviserinfo.sec.gov/firm/summary/333974.